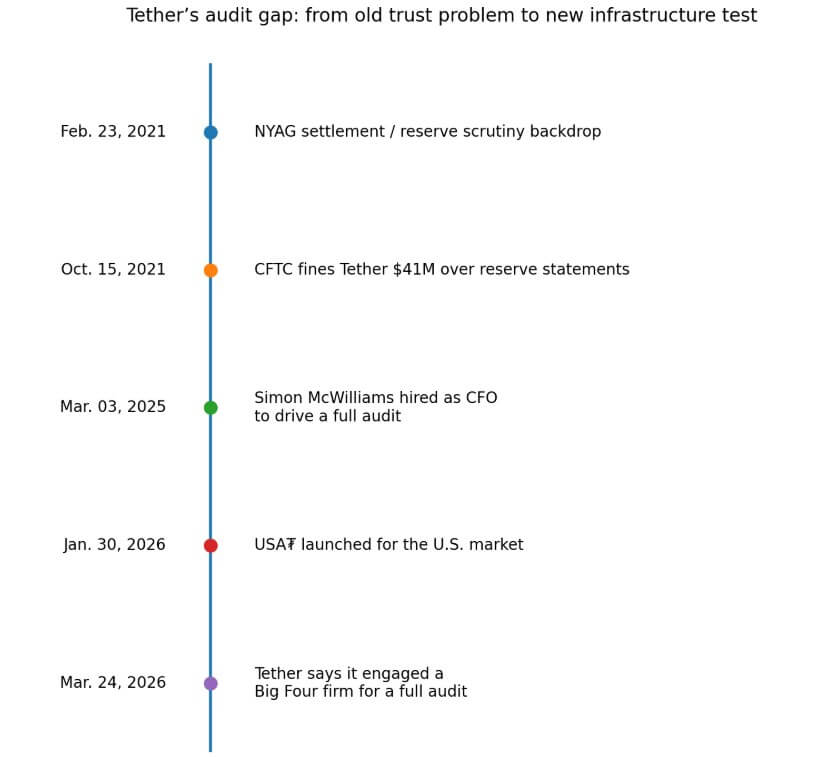

For years, the shortest line of attack against Tether was the demand for a fully independent audit.

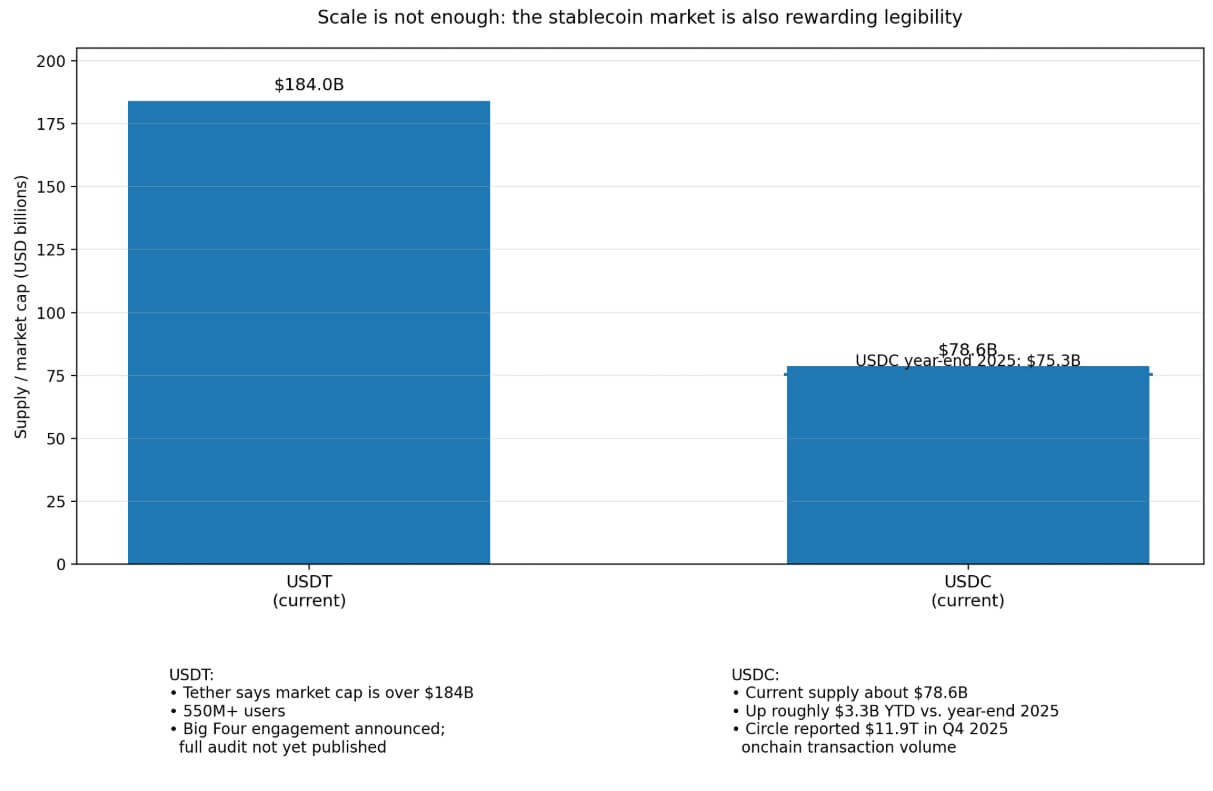

The audit never came and the company absorbed the reputational costs without visible damage to its position. USDT exceeded $184 billion in market capitalization, reached more than 550 million users and became the dominant liquidity layer in global crypto markets.

On March 24, Tether announced that it had formally engaged a Big Four firm for its first full independent audit of financial statements.

This came after Paolo Ardoino, CEO of Tether, said this Crypto Slates Editor-in-Chief nearly two years ago, he said he was actively trying to get a “Big Four” firm on board, but found the political and regulatory environment in the US made this extremely challenging. According to him, the lack of a Big Four audit was not due to a lack of effort by Tether.

At the time, he said regulatory pressures, such as Senator Warren’s call for accountants to avoid crypto companies, made it difficult for Tether to obtain a full audit of a Big Four company. He expressed confidence in Tether’s continued efforts to prove its legitimacy and financial health, which finally appear to be paying off.

Speaking about the “risk” for an accountant to take on Tether as a client, and the failed attempts to bring in a “Big Four” firm after “harsh” treatment by US lawmakers, he said:

“Look, really openly attesting to a stablecoin, especially if the stablecoin is called Tether, naturally involves a lot of attention and a lot of risk management. And rightly so, right? […]

We have been trying to get a Big Four auditor to do the full audit… it is still our top priority.”

👀 @paoloardoinoCEO of @Tether_to, talk to @CryptoSlate‘S @akibablade & @jvs_btc in his most transparent and open interview yet.

Paolo reveals information about the inner workings of Tether’s audits, the competition, FUD, and where Tether has been naive over the years.

🚨 MUST WATCH 🚨 pic.twitter.com/FZcLJO4tM0

— CryptoSlate (@CryptoSlate) June 28, 2024

The debt that was never repaid

The historical record seemingly gave Tether’s critics lasting ammunition.

In 2021, the CFTC ordered the company to pay $41 million for misleading statements claiming that US dollars fully supported USDT.

New York’s attorney general said Tether and Bitfinex made false statements about reserves while hiding about $850 million in losses. These findings gave Tether a confidence discount that never fully retired the quarterly certificates, even as the USDT supply continued to rise.

Tether’s public preparations for this announcement date back at least a year, while Ardoino’s comments suggest it goes back even further.

In March 2025, the company hired Simon McWilliams as CFO with an explicit mandate to conduct a full audit, framing that work as part of a broader push in the institutional financial system.

The March 24 announcement is the first concrete sign that efforts have reached a formal commitment.

The company itself drew the relevant line, saying that attestations represent the current standard for stablecoins and that the audit takes them “beyond this benchmark.”

This framing is a direct acknowledgment that the benchmark is no longer sufficient for the company’s desired trajectory.

The sanitary facilities are built around it

The urgency behind Tether’s audit push becomes clearer when compared to what major financial institutions are now building.

DTCC has announced that NSCC plans to begin 24×5 trade processing on June 28, pending regulatory approval, calling it a fundamental step toward a more continuous market.

NYSE is designing a tokenized venue built around 24/7 operations, instant settlement, and stablecoin-based financing.

Nasdaq has proposed tokenization as the path to an “always-on financial ecosystem.” BMO, CME Group and Google Cloud announced a tokenized cash platform that allows institutional clients to continuously move value for margin, collateral and settlement.

This constellation of announcements describes a reorganization of the market around continuous operation and symbolic dollar movements.

| Institution / project | What is being built | Why it raises the bar for stablecoins |

|---|---|---|

| DTCC/NSCC | 24×5 trade processing and market infrastructure that is open longer | Longer trading windows increase the need for dollar instruments that can move reliably outside of traditional banking hours |

| NYSE tokenized platform | A location designed around 24/7 operations, instant settlement, and stablecoin-based financing | Stablecoins are brought closer to the core functions of financing and settlement, rather than remaining just liquidity instruments for exchanges |

| Nasdaq tokenization push | An ‘always-on financial ecosystem’ built around tokenized financial assets | Stablecoins are increasingly assessed on whether they can function within a continuous, interoperable capital markets environment |

| BMO / CME Group / Google Cloud | Tokenized cash for real-time margin, collateral and settlement workflows | If stablecoins or tokenized dollars are used for margin and collateral movements, reserve quality and auditability become more important |

| Stablecoin issuers in general | A shift from crypto trading collateral to settlement-quality cash rails | The closer stablecoins get to market piloting, the less tolerance institutions have for unresolved transparency questions |

| Market implication | Stablecoins compete for the familiar ‘cash leg’ in tokenized markets | Winners are likely to be judged not only on scale, but also on how easily counterparties, platforms and institutions can explore and integrate them. |

DTCC’s own materials carefully distinguish between 24×5 and 24×7 and describe the transition as staged.

The bar is being raised in ways that make the identity of the dollar sign more important than it was when stablecoins existed primarily to finance crypto transactions.

In a market where NYSE explicitly envisions stablecoin-based financing and BMO is building infrastructure for real-time margin and collateral movements, counterparties will ask tougher questions about the quality and auditability of reserves.

A stablecoin used as settlement-grade money is controlled at a different level than a coin used to move between exchange accounts.

What institutional readability can buy

Circle’s numbers provide the clearest available evidence of what happens when a stablecoin makes itself easier for institutions to understand and control.

Circle reported $75.3 billion in USDC circulation at the end of 2025 and $11.9 trillion in on-chain transaction volumes in the fourth quarter of 2025.

Current supply is about $78.6 billion, which represents growth of roughly $3.34 billion by 2026, and that growth reflects multiple factors.

USDC works best here as an illustration of what institutional readability can unlock.

The more useful observation is that the market has already shown that compliance, clearer reserve disclosure, and easier institutional integration can translate into meaningful scale.

Tether’s audit push reads like an attempt to access the same pool of institutional demand, and the January launch of USA₮ reinforces that reading.

Anchorage Digital Bank issues USA₮ for the US market, with Cantor Fitzgerald serving as reserve custodian and preferred primary dealer, while USD₮ continues to be issued globally.

That architecture looks like an early attempt at restructuring for a world where different markets apply different standards to stablecoin issuers.

A qualifying match

In the bull scenario, Tether delivers a clean full audit and uses that result to close its institutional trust gap, right as tokenized security securities, 24×5 clearing, and tokenized cash networks move from announcement to operation.

The audit will be the qualifying step that keeps USDT relevant to the next generation of market infrastructure.

The supporting evidence is the number of major incumbents that have already laid the rails: DTCC, NYSE, Nasdaq, BMO, CME and Google Cloud are all building a more continuous, tokenized market, and each of these projects needs a credible dollar leg.

In the bear case scenario, the audit drags on and the company remains nameless. No timetable surfaces.

In that scenario, marginal institutional flows continue to move to issuers that are already easier to monitor, and to bank-linked tokenized cash systems that have an implicit reserve guarantee through their issuer.

USDT retains its grip on crypto-native liquidity, but Tether is excluded from the more regulated settlement workflows that the largest incumbents are building.

That outcome is more plausible than it was two years ago precisely because NYSE and BMO are designing infrastructure with explicit stablecoin financing components, creating real switching costs for stablecoin issuers that can’t pass institutional due diligence.

Tether’s real audience for this announcement could be the next generation of operators, such as clearing firms, broker-dealers, tokenized securities platforms and exchange operators, who are now deciding which dollar tokens can be integrated into their infrastructure.

The missing audit becomes a qualification issue in a market where stablecoins are being evaluated as candidates for the dollar leg of continuous clearing, real-time margin, and always-on settlement.

The oldest unanswered question about the world’s largest stablecoin comes with a different set of costs than when stakes were limited to the liquidity of crypto exchanges.

Tether’s announcement is the first step in closing that gap.