Ripple CEO Brad Garlinghouse sidestepped a direct question about whether the company would ever buy a bank, using the moment to reiterate Ripple’s institutional-first strategy and argue that clearer U.S. rules are already unlocking demand for stablecoins and XRP Ledger-based payments.

Garlinghouse spoke with James Hasso at the Economic Club of New York on February 18 asked whether Ripple directly acquires a bank or forges closer partnerships as it works with major financial institutions and builds out its stablecoin business.

“I’m going to dodge part of your question answer,” Garlinghouse said, before addressing why Ripple has historically embraced banks rather than positioning itself against them.

What is Ripple’s plan?

Garlinghouse described Ripple’s stance as deliberately contrarian to early crypto culture. “Ripple took a contrarian and controversial strategic approach to the way we went to market early on and that made us unpopular in crypto,” he said. “Ripple said early on that banks are our customers. If we want these technologies to have the greatest impact on the greatest number of people, banks are the point of contact for people in their financial services relationships.”

Related reading

He contrasted that with what he described as crypto’s initial instinct to build outside the existing system. “The early days of crypto were very anti-banking, anti-government. Let’s build a parallel universe,” Garlinghouse said. “Ripple always believed that we would bridge what we would now call tradfi or traditional finance and defy decentralized finance.”

This bridge-building claim also anchored his response to Ripple’s regulatory stance around its stablecoin business. Garlinghouse said Ripple launched RLUSD 13 months ago and claimed it is now “about number five” among the largest stablecoins – a result he linked to leaning on oversight rather than avoiding it.

Garlinghouse highlighted a trust license from the New York Department of Financial Services and a conditional OCC charter, characterizing the latter as “belt and suspenders” for the stablecoin business. “We think our unique position, as you know, is almost over-regulated,” he said.

“But we want that… because we work with institutions, we want them to see us as someone who goes above and beyond to make sure that there is that level of oversight, so there are no questions… is the stablecoin supported on a one-to-one basis? [and]…the testimonials on a regular basis about this support.”

Then came the cleanest non-answer of the session. “And I’m going to skip the question: Will we ever buy a bank? They’re customers,” Garlinghouse said.

Related reading

Garlinghouse wondered whether additional U.S. legislation could speed up adoption, pointing to an earlier example: “The Genius Act was the stablecoin legislation that was passed…President Trump signed it in late July or early August,” he said. “That was certainly an unlocker… we definitely saw a big increase in stablecoin activity after this became law.”

He argued that a similar effect could occur if the Clarity Act passes, as clearer definitions would give boards, CFOs and banks more room to maneuver. For businesses, he emphasized the operational utility – especially the “24/7 ability to move stablecoins” – arguing that “sometimes it’s important to be able to make a payment on a Sunday afternoon.”

Garlinghouse said Ripple has retained its commercial focus in payments because its value proposition is simple: faster, cheaper settlement. On tokenization, he was supportive but selective, noting friction in traditional settlement cycles such as “T+3” and “T+1,” while also warning that some projects feel like “a technology in search of a problem.”

Pointing to BlackRock CEO Larry Fink as a prominent advocate, he said Fink believes a “huge percentage of assets will be tokenized,” adding, “I agree with him.” But Garlinghouse emphasized that execution will be “vertical by vertical,” arguing that domain experts, not Ripple, should drive industries it doesn’t understand, such as insurance.

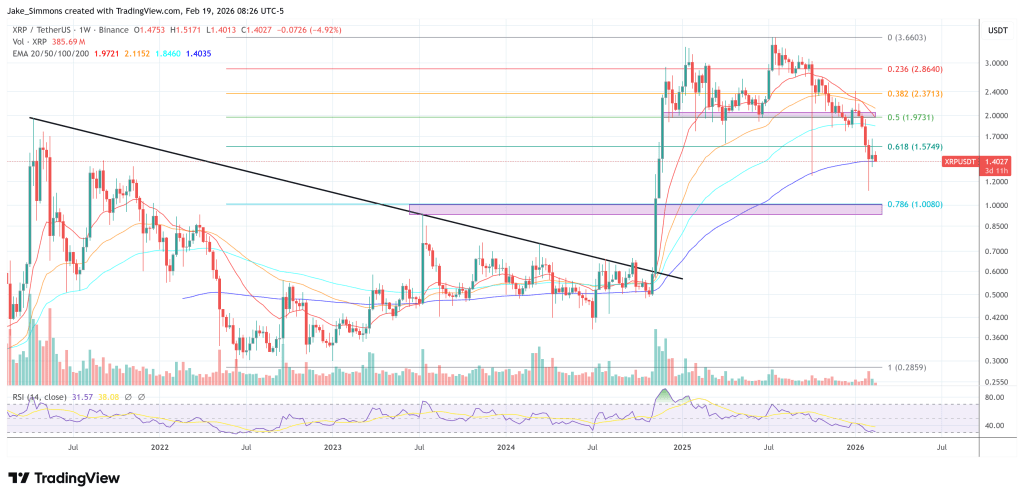

At the time of writing, XRP was trading at $1.4027.

Featured image from YouTube, chart from TradingView.com