Reason to trust

![]()

Strictly editorial policy that focuses on accuracy, relevance and impartiality

Made by experts from the industry and carefully assessed

The highest standards in reporting and publishing

Strictly editorial policy that focuses on accuracy, relevance and impartiality

Morbi Pretium Leo et Nisl Aliquam Mollis. Quisque Arcu Lorem, Ultricies Quis Pellentesque NEC, Ullamcorper Eu Odio.

A radical new research report from Ben Harvey and Will Clemente III, commissioned by market maker Keyrock, projects that Bitcoin could reach $ 160,000 by the end of 2025 only if the capital structure that supports Bitcoin Treasury Companies (BTC-TCS) remains intact. The research“BTC treasuries discovered: premiums, leverage and the sustainability of exposure to proxy”, dissects the capital structures, market impact and debt profiles of the fast-growing cohort of “Bitcoin Treasury Companions” (BTC-TCS), led (the renamed microsstrategie).

The impact of Bitcoin Treasury companies

Harvey and Clemente Open with a surprising figure: “Bitcoin Treasury companies have collected around 725,000 BTC, equal to 3.64 percent of the entire BTC offer.” Much of those Hamstares is with the 597,000-coin trove of the strategy, but the analysts follow more than a dozen follow-up players-from Marathon Digital and Metaplanet to newer participants such as twenty-one capital-that combined exposure now surpasses more than half.

Related lecture

Nevertheless, the head forecast of the report is explicitly conditional. Keyrock’s bull’s case allows a probability of thirty percent that global liquidity remains the same, accelerates institutional demand and Bitcoin Rallies fifty percent beyond today’s level, “push BTC to more than $ 160 K by Eoy.” That outcome is based on the fragile flywheel of Net-ASCHET value premiums: BTC-TC shares still trade on average by seventy-three percent premium to the dollar value of the coins they are guardian. Thanks to those premiums, Boards can give new shares “accretief”, convert sentiment into new BTC, and – cross -breeze – serve the $ 33.7 billion in debts and preference shares that the sector has sustained to finance the purchase bench.

No company illustrates the reflexive loop better than strategy. Since August 2020, Michael Saylor has driven eleven-fold Bitcoin-Per-Share (BPS), an annual sixty-three percent run rate that the 6.7 percent CAGR dwarf it is needed to justify the current ninety percent NAV premium of the company. “If an investor is of the opinion that the BPS growth rates of the long-term strategy will remain,” the authors claim, “keeping MSTR would be much cheaper in BTC terms than keeping spot BTC.” Nevertheless, Calculus assumes that the stock premium will continue to float; If sentiment runs, the dilution watering from declaration to penalties will fold at night.

Debt running times are the following stress point. BTC-TCS owes a wall of convertible notes in 2027-28. Harvey and Clemente calculate that only strategy has spent $ 8.2 billion of the $ 9.5 billion in debts; Marathon follows $ 1.3 billion. Most instruments have zero-to-drag coupons and conversion prices far below the current equity level, but a deep Bitcoin tafting drawing could stimulate shares under those strikes, allowing companies to repay in cash or refinancing in far conditions. “Because many BTC-TC valuations are closely correlated with Bitcoin prize performance,” warn the authors, “can lower a sharp BTC recording, which increases the risk that conversion thresholds will be violated.”

Related lecture

The report splits the universe in Cash-Flow generative names such as Metaplanet, Coinshares and Boyaa Interactive milk with eight or more quarters of runway and capital-dependent players such as Marathon, Nakamoto and Defi technologies, which can get a thinning of three percent per quarter. If those premiums compress, equity issue are ‘purely diluting’, and Finury companies can be forced to sell Bitcoin, which undermines the Proxy thesis that justifies their existence.

The basic store

The basic case of Keyrock, to which it assigns the highest chance, provides in Bitcoin, 2025 ends around $ 135,000, with NAV premiums cooling to a range of thirty to sixty percent. In that environment, well -managed treasuries still perform well, but the lever trade loses its shine. The bear scenario-has the lowest but non-trivial opportunities assigned combining a Bitcoin covering of twenty percent with an abundance of new treasury lists that flood the market with offer. In that world, premiums, refinancing windows slam shut up and “the entire investment case for BTC-TCS comes under pressure.”

Harvey and Clemente do not reject the BTC-TC model; On the contrary, they frame it as an overlay with a high beta that strengthens both the upward and the solvency risk that is inherent to Bitcoin itself. They credit Saylor’s “Bitcoin Yield” thesis-with the help of premium-fined issues of shares on composite coin interests-and a demonstrable effective strategy to date, but warn that it depends on a delicate balance of Bullish Sentiment, cheap capital and closed version. “The NAV premium is of the utmost importance here,” concludes the study, “assuming a BTC-TC has no core company that can cover debt payments, or is completely free of debt payments.”

Whether Bitcoin can sprint to $ 160,000 until 31 December, depends less on hash-rate projections or macro modeling than on the continuous belief of stock investors willing to pay a dollar fifty for a dollar embedded BTC. If those investors blink and premiums blink or convertible running hours collide with a wide risk-off shift-zou the leverage that has propelled so far, treasury companies can turn around, so that “one of the best performing shares on the planet” is changed in the most busy exit of the market. For now, Keyrock’s research has a simple countdown: hold the line and the path to price discovery remains intact; Loss it and the proxy trade could relax long before the fireworks of the new year.

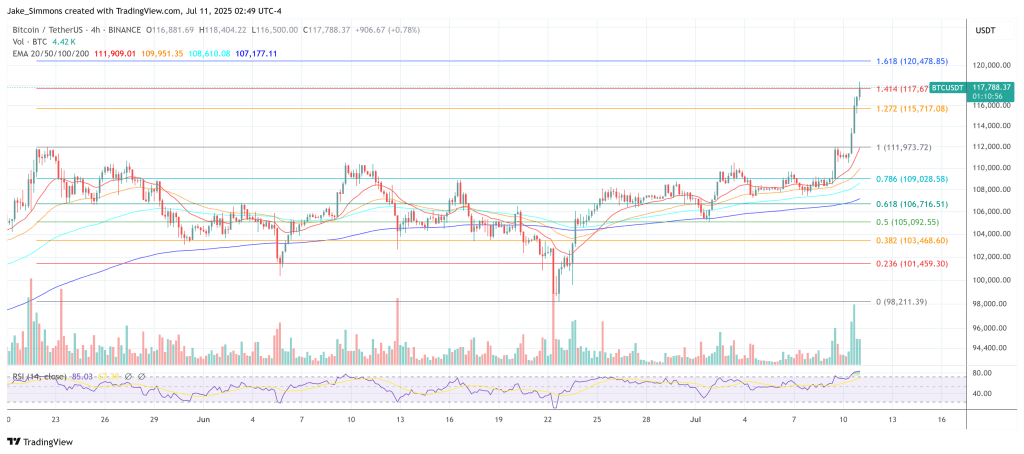

At the time of the press, BTC traded at $ 117,788.

Featured image made with dall.e, graph of tradingview.com