Circle’s biggest selling point could be its biggest risk. On-chain researcher ZachXBT’s “Circle Files” claim that the USDC issuer has applied its freezing powers inconsistently.

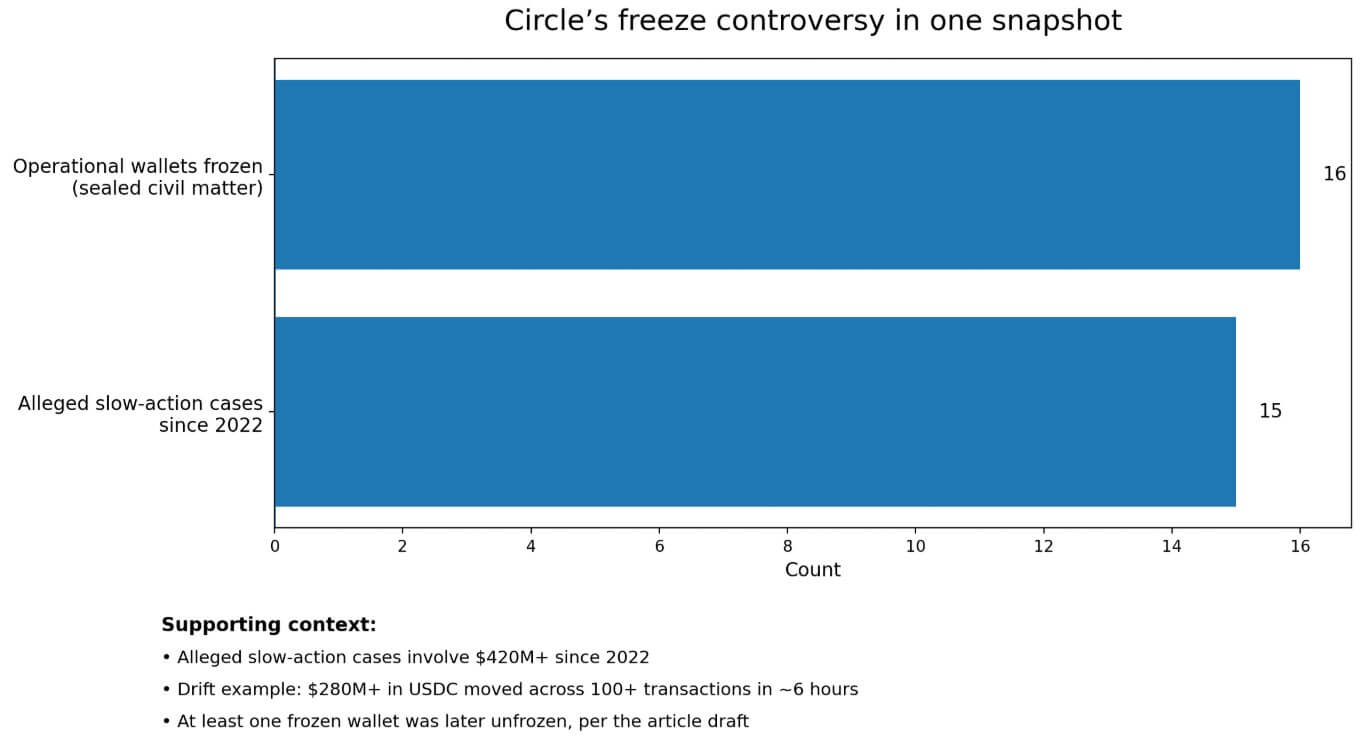

Circle was too slow in 15 cases involving more than $420 million in allegedly illicit funds since 2022, yet broad enough to capture 16 operational business portfolios in a sealed US civil case. The wallets were linked to exchanges, casinos and forex services that ZachXBT said appeared disconnected.

Why this is important: USDC is an important settlement tool in cryptocurrencies and is widely used by exchanges, traders, payment flows and DeFi protocols. Circle’s freeze decisions extend beyond individual legal disputes or hacking responses and set the limit for how much operational risk companies accept when holding or moving dollars up-chain.

The company later unblocked at least one of those wallets, which belonged to Goated.com, further raising questions about how closely Circle reviews the addresses it puts on the block list.

This sequence of ‘slow in the case of theft, drastic in civil proceedings’ comes at a difficult time.

USDC had approximately $77.2 billion in circulation as of April 3, out of a total stablecoin market of nearly $316.8 billion, accounting for approximately 24.5% of that pool. In one of the cases cited by ZachXBT, the Drift exploit, over $280 million in USDC was moved across more than 100 transactions in about six hours.

At that scale and speed, the gap between ‘can freeze’ and ‘frozen in time’ is the whole practical question.

The legal stack that Circle built

Circle’s control surface has real teeth on the chain. The EVM stablecoin contract includes a blocking function under a blocking role, and addresses on the blocking list cannot transfer or receive tokens.

Circle has designed the contract to be both pauseable and upgradeable.

That architecture existed long before this controversy arose, and Circle’s Access Denial Policy codifies when that power is activated.

Circle can block individual addresses on any blockchain where its stablecoins are issued. Once declined, the associated balance cannot be moved back up the chain.

The policy freezes limits to two limited triggers: when Circle, in its sole discretion, determines that failure to act would jeopardize network security or integrity, or when a valid legal order from a recognized U.S. or French authority requires it.

Chargebacks require formal confirmation that the legal obligation or security basis no longer applies.

The USDC terms add a second layer. Nothing in these Terms obligates Circle to maintain, verify or determine Users’ USDC balances.

However, Circle also reserves the right to block addresses and freeze associated USDC that Circle determines in its sole discretion may be associated with illegal activity.

The Circle Mint User Agreement continues: Circle may suspend accounts at its sole discretion, including pursuant to court order, and may limit redemptions or transfers where prohibited by law or court order.

Access denial policies sound narrower and more formally rules-based, blocking sounds exceptional, linked to security events or legal coercion. The broader USDC terms and user agreement give the issuer significantly more leeway.

Circle’s legal terms provide the issuer with significantly more leeway than the limited design of the denial of entry policy implies. When legal processes and user continuity collide, Circle’s proprietary hierarchy prioritizes compliance and publisher control.

| Document/layer | What Circle says, it can do | Why it matters |

|---|---|---|

| EVM stablecoin contract | Addresses on the blocked list cannot transfer or receive tokens; contract is pauseable and extensible | Shows that Circle’s control exists directly in the token architecture |

| Access denial policy | Can block addresses in chains; freezes related to network security/integrity or valid US/French legal orders | Frames freeze so narrow and exceptional |

| USDC Terms | Circle may, at its sole discretion, block addresses and freeze USDC associated with suspected illegal activity | Expand Circle’s playing space |

| USDC Terms | Circle has no obligation to track, verify or determine the origin of users | Limits what users can expect from Circle for them |

| Circle Mint User Agreement | Circle may suspend accounts at its sole discretion, including pursuant to court orders | Shows that compliance can override user continuity |

Where criticism bites

The 16 wallet incident illustrates why operators are now experiencing problems with this hierarchy. Circle’s freeze power was carried out quickly and broadly when a sealed civil case arrived on his desk.

ZachXBT’s “Circle Files” claim that the same force has moved too slowly over 15 theft cases since 2022, and the Drift Window, $280 million plus over 100 transactions in six hours, is the starkest example because the scale and number of transactions appeared on the chain in real time.

The GENIUS Act, passed in July 2025, created a US regulatory framework for payments stablecoins, treating USDC-type products as regulated financial infrastructure.

The OCC’s implementation proposal has a May 1 comment deadline. The March 2026 FATF report emphasized that regulators should assess whether blockchain analyzes and audits deliver tangible enforcement results, and that timely public-private coordination is crucial for asset recovery.

That is the precise standard that ZachXBT and the operators involved are now applying to Circle.

Circle markets USDC as fully backed, transparently managed, and the world’s largest regulated stablecoin. Circle’s own 2026 Internet Financial System report cited over $50 trillion in cumulative USDC settlements, 40% of stablecoin transaction volume and 29% of stablecoin circulation as of September 2025.

At that scale, the frozen administration has systemic weight, and the scrutiny it now faces reflects the infrastructure role that Circle has claimed for itself.

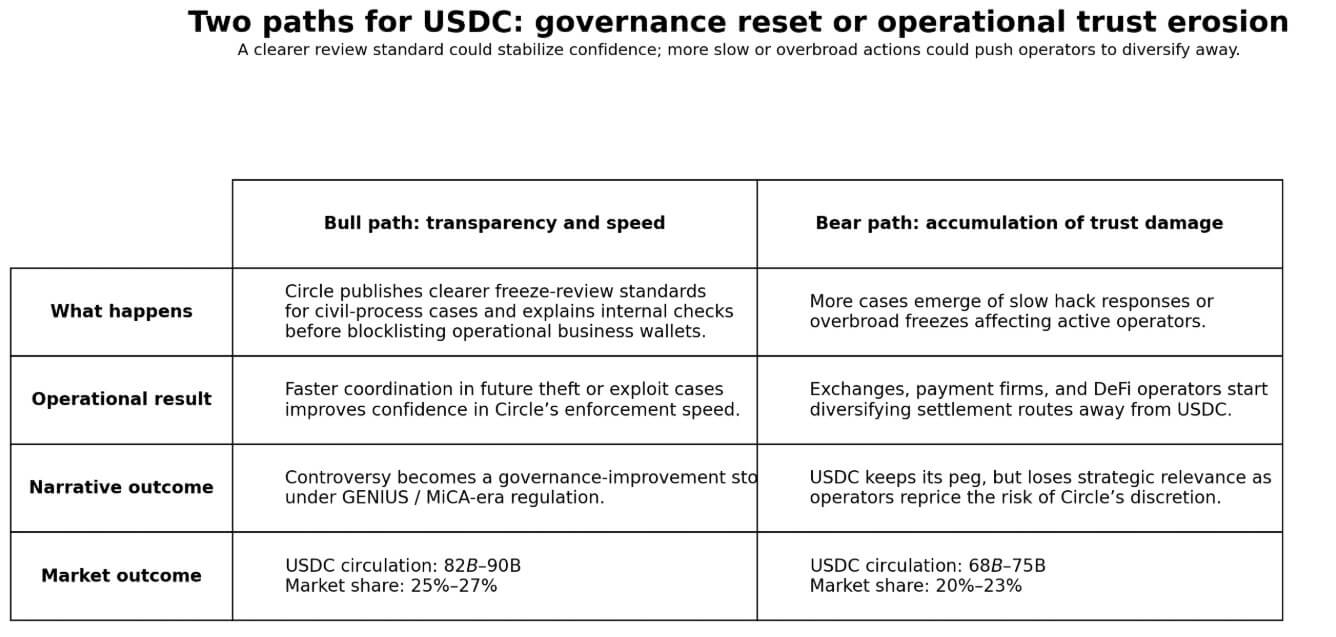

Two paths for Circle

The bull’s path runs through transparency and speed.

If Circle publishes a clearer review standard for freezes related to civil proceedings, detailing what triggers internal review before Circle places operating corporate wallets on the block list, and demonstrates significantly faster coordination in future hack response situations, the controversy will become a board maturing story.

In that scenario, regulation under the GENIUS framework and MiCA rewards the most institutionalized issuer, and USDC circulation could recover to the $82 billion to $90 billion range, with a 25% to 27% market share.

The 16-wallet incident, in which Circle had already recovered one wallet, would be the moment when Circle clarified its process.

The bear trail runs through accumulation. Examples of slow responses to hacks or excessive freezes on civil lawsuits are emerging, and operators holding USDC in hot wallets, such as exchanges, payment companies, and DeFi protocols, are starting to diversify settlement routes.

A stablecoin can maintain its $1 peg while losing strategic relevance, and operators diversifying outside of Circle would not trigger a depeg alert.

Tether, PYUSD, and an ever-expanding field of issuer-specific tokens each give operators a route away from Circle’s control stack.

As a result, USDC circulation is moving toward a range of $68 billion to $75 billion and a 20% to 23% market share as companies reassess the operational risk arising from Circle’s judgment.

The next checkpoint will come through operational performance, depending on how quickly Circle responds to the next hack, how quickly it restores blocked-listed wallets, and whether freezes hit operators for a clearer reason than the previous batch.

The OCC comment window closes on May 1 and the regulatory regime for payment stablecoins is taking shape while this dispute lives.

The market now wants to know whether the compliance used by the Circle model protects users or concentrates power in an issuer whose rating standards cannot be seen by operators.