- Bitcoin holders should be wary in the short term due to increased selling pressure around the halving.

- The halving event was likely not priced in, but that doesn’t guarantee the same returns from this BTC cycle as previous ones.

Bitcoins [BTC] The halving did not immediately lead to a massive sell-off, as some market participants feared. While things could change later this week, the $60,000 support zone was defended on April 19.

Since the dip to $59.6k, prices are up 9% at the time of writing.

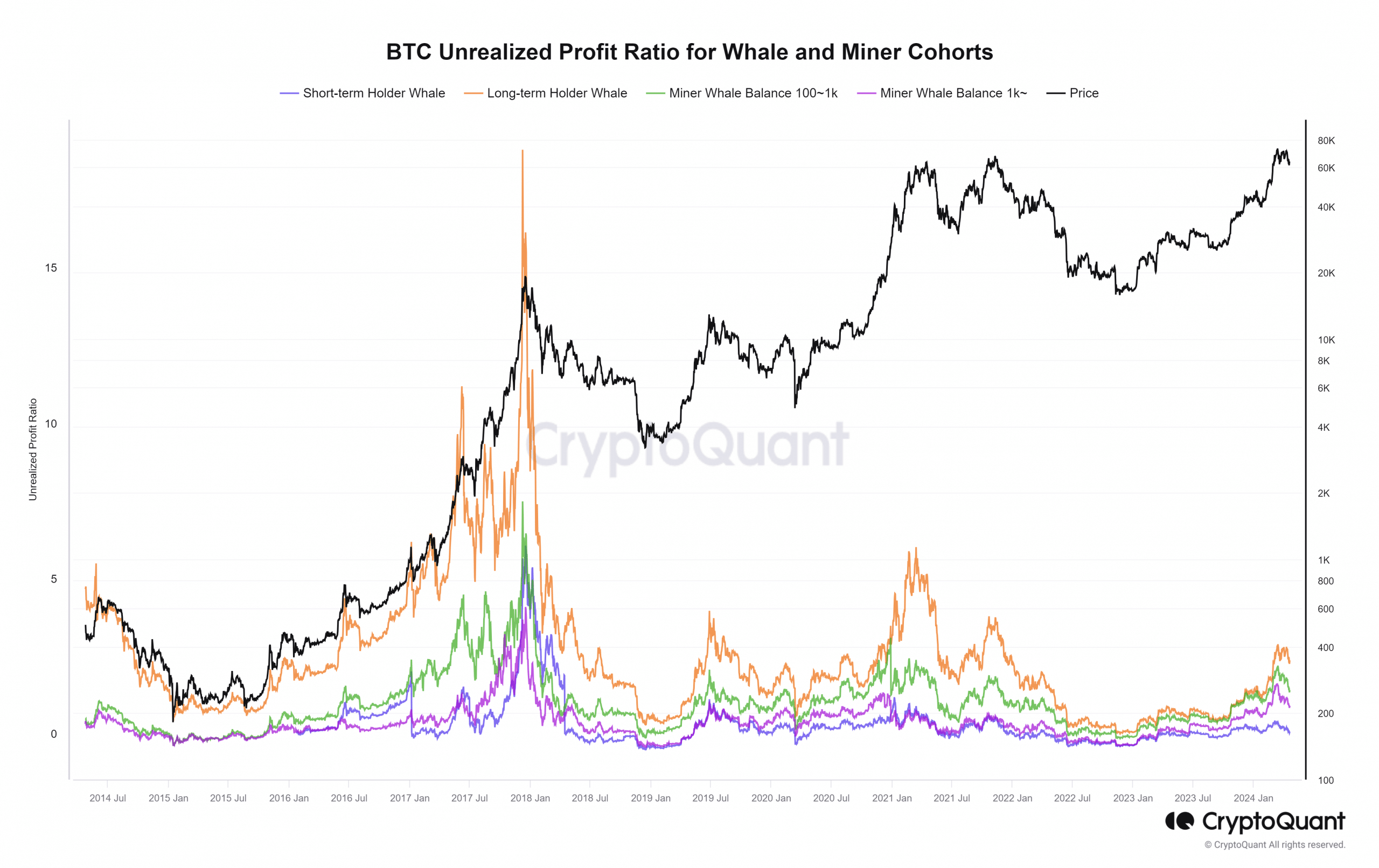

In a message on X (formerly Twitter), CEO of CryptoQuant Ki Young Ju have pointed out that we are not yet close to the top of this cycle. The Unrealized Profit Ratio metric showed that whales only made a 234% profit in the long term.

The 2021 run had long-term whales with a 599% gain at the metric’s peak in February 2021. Although BTC made a new high later that year, the unrealized gains metric couldn’t match it.

Playing the long game

Comparing the 2020-2021 cycle to the 2017-2018 rally, we see that the whales’ long-term gains in 2017 were over 1700%. The respectable figure of 599% pales somewhat in comparison.

This raises the question of a further decline in whale profits during the top of this cycle. Therefore, expectations of Bitcoin reaching $200,000 may be ambitious, but only time will tell.

With a reading of 286% in mid-March, bulls would be hoping that the halving would boost these numbers. As Ki Young Ju says, this may not be enough gain to end the cycle.

Crypto analyst Ali Martinez drew attention to the sentiment surrounding Bitcoin as it reaches its peak. Based on the NUPL metric, we have the “euphoric” phase that usually comes with a Bitcoin summit.

Short-term threats

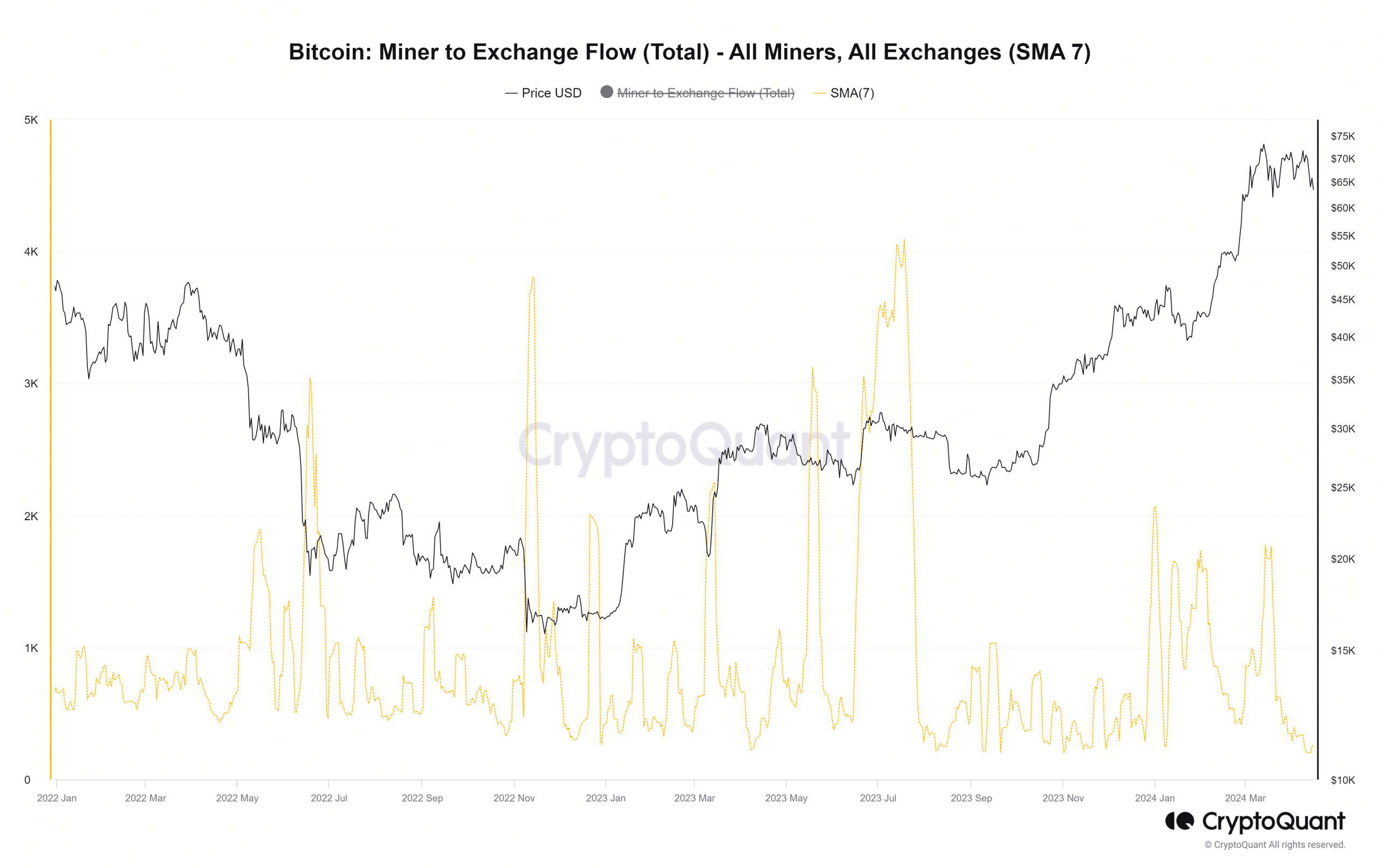

While the long-term outlook calls for higher prices, there is room for volatility in the short term. Data from CryptoQuant shows that miners sent less BTC to exchanges last month.

The declining 7-day simple moving average of the flow of miners to exchanges was evidence of this.

One possibility is that miners are hoarding Bitcoin to sell after the halving, as their rewards would then be halved. This in turn could put significant downward pressure on the market.

Furthermore, there have been indications of weakened demand for Bitcoin in recent weeks. Liquidity inflows peaked on March 12 and have declined in recent weeks.

Over the past two weeks, Bitcoin prices fell from 10% to 15%, but ETF inflows were not stimulated. It indicated a saturation in demand for US-listed Bitcoin ETFs at the moment.

The halving must be priced in, common sense says

The halving event on April 19 (or the early hours of the 20th if you’re in the Eastern Hemisphere) is an event that the entire market has known about for years.

The aftermath isn’t so simple as the rewards drop to 3,125 BTC per block mined.

At the heart of the problem is the multitude of other factors at play, all of which revolve around supply and demand, and public sentiment towards Bitcoin.

The argument that the event has been priced in because the market has known about it for centuries may be redundant. argues on-chain Bitcoin analyst Willie Woo.

A shift in public sentiment occurs relatively late in Bitcoin’s cycle. Bitcoin usually attracts public attention just before or after the NUPL euphoria phase.

This cycle may be different because of the ETFs, but the argument against pricing is still valid.

We simply haven’t had the capital inflows that will eventually price Bitcoin correctly. As things stand now, the asset appears vastly undervalued over the long term.

Read Bitcoin’s [BTC] Price forecast 2024-25

A more pessimistic view would lead to the conclusion that this cycle would be much shorter and not as parabolic as the previous ones.

In both scenarios, the roller coaster ride has not yet reached its quota of airtime. So tie up and hold on.