Bitcoin is at a ‘critical point’, with traders divided between two known scripts: a full capitulation event, or the early innings of a sustainable bottoming process. In a February 15 video explainer, CryptoQuant analyst Maartunn argued that the data is starting to line up for the latter, but with an obvious caveat that any bottom will be a grind rather than a snapback.

Has the Bitcoin Bottom Been Reached?

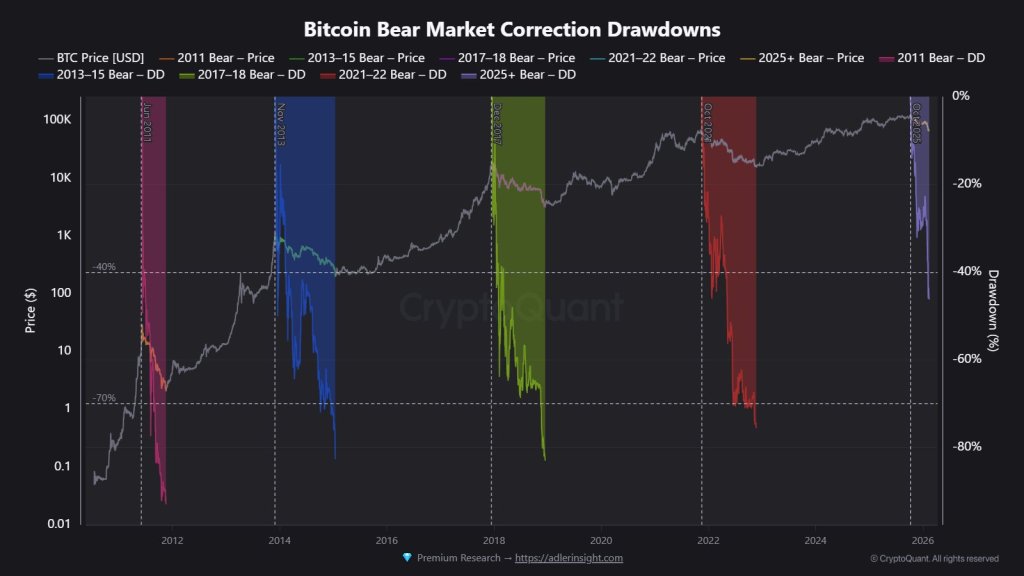

Bitcoin is currently trading roughly 50% below its all-time high, a decline that seems severe in itself, but is still smaller than the 70%-plus declines seen in previous bear markets, Maartunn said. The more useful question, in its formulation, is not whether the market can decline, but whether the ingredients that usually precede a turn will appear.

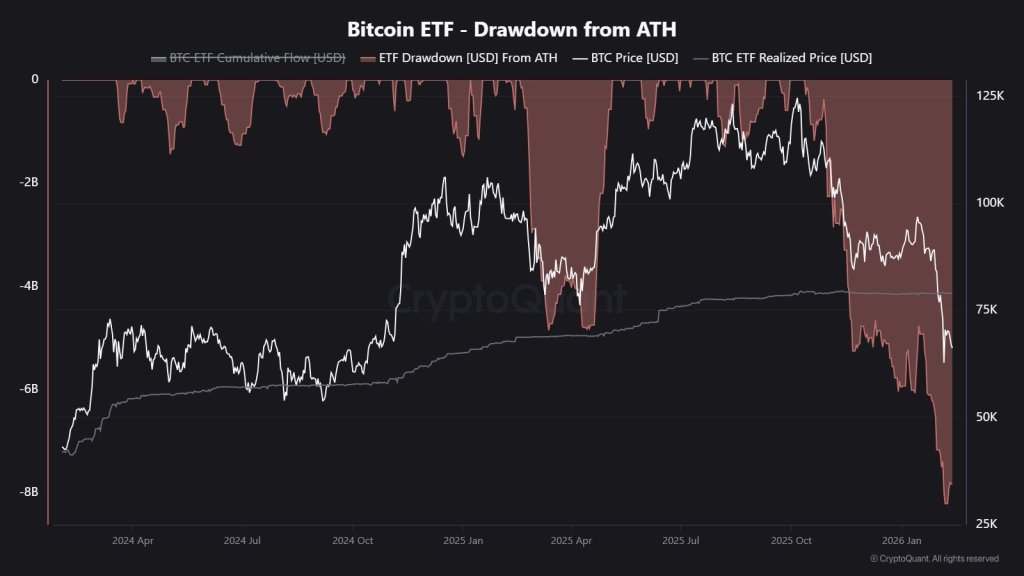

Maartunn first points to what he describes as “structural selling pressure” associated with spot ETFs. According to his numbers, the new spot ETFs have posted an $8.2 billion decline from their peak positions, “the largest on record,” creating continued selling pressure. He adds that the current price is about 17% below the average purchase price for ETF holders, leaving a significant portion of that cohort underwater and potentially incentivizing them to reduce exposure.

Related reading

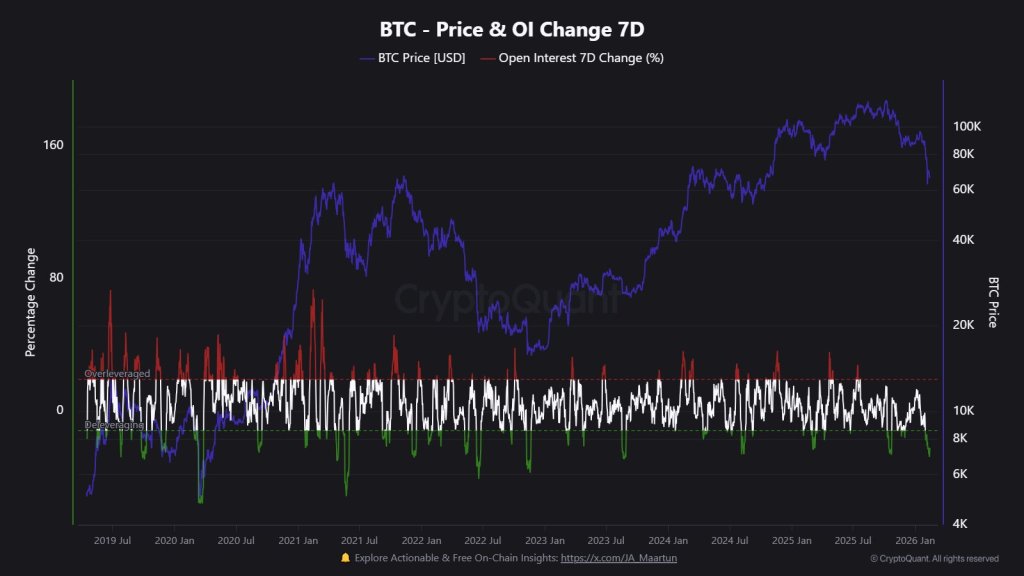

He then links that flow story to a mechanical reset in derivatives. Open interest has “decreased by more than half,” from $45.5 billion to $21.7 billion, with a 27% drop in open interest in the past week alone. Maartunn describes this as a large-scale deleveraging event, painful in real time, but historically consistent with conditions that allow a bottom to emerge.

“Look, it’s absolutely painful for anyone who has too much debt, but getting rid of all that speculation is an absolutely necessary step to form a true sustainable market bottom,” he said. “This is a signal of a major excess of speculative excesses.”

To gauge whether the pullback translates into capitulation-like stress, Maartunn focuses on short-term holders. He cites the MVRV ratio for short-term holders of 0.72, implying that the average short-term holder is down about 28%, “deeply underwater” as a group. According to him, that’s not a routine reading: It’s the lowest level since the July 2022 bottom, and a band that’s historically aligned with periods of maximum financial pain.

“This level of financial stress is historically quite rare, and it usually happens during periods of major capitulation,” Maartunn said. “Of course, could this ratio go any lower? Absolutely. But what history shows us is that when we reach these levels, the risk-reward profile for Bitcoin starts to look a lot better.”

Related reading

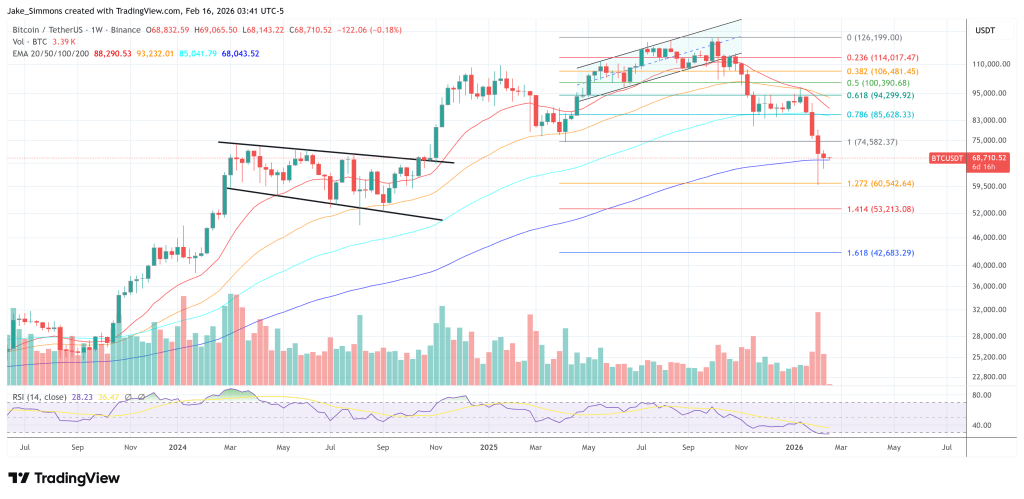

Maartunn also sees the current structure as a retest of a key support cluster – where the all-time high from the previous cycle intersects the upper limit of an older trading range – a zone that has often mattered in previous cycle transitions. From there he turns to time-based analogs, suggesting that previous bear market episodes imply a broad period between June and December 2026, with the last two cycles clustering most strongly between September and November.

His closing point is that lows are rarely one-day events. According to him, ETF-driven structural selling, the debt crisis, stress among short-term holders and the retesting of key levels could all co-exist within a longer bottoming process – with sentiment being the final word.

“A real bottom in the market… usually characterized by apathy,” he said. “When social media engagement is completely dead, your timeline is silent, and honestly, no one seems to care anymore. That period of total disinterest is often the point of maximum financial opportunity.”

Overall, the implication of Maartunn’s framework is simple: the data may shift towards early bottoming signals, but the corroborating evidence, particularly around flows and sentiment, could still arrive in stages, with volatility and further stress testing in the future.

At the time of writing, Bitcoin was trading at $68,710.

Featured image created with DALL.E, chart from TradingView.com