Bitcoin briefly regained the psychological $80,000 level during early Asian trading hours on May 4, the first time since February, amid the quiet upward march of recent weeks.

Data from CryptoSlate showed the top crypto hitting an intraday high of $80,529 before falling back to $79,621 at the time of writing.

However, what appears to be a triumphant milestone on a price chart masks a deeply conflicted market structure under the hood.

This is because the major cryptocurrency’s return to this threshold is less a pure bullish breakout than a high-stakes test.

Still, market analysts noted that BTC traders are currently trying to determine whether recovering institutional demand in the spot market can overpower a still hostile macroeconomic environment marked by tensions in the Middle East, an aggressive Federal Reserve handover and a derivatives market that remains deeply skeptical.

An aggressive, but vulnerable escape attempt

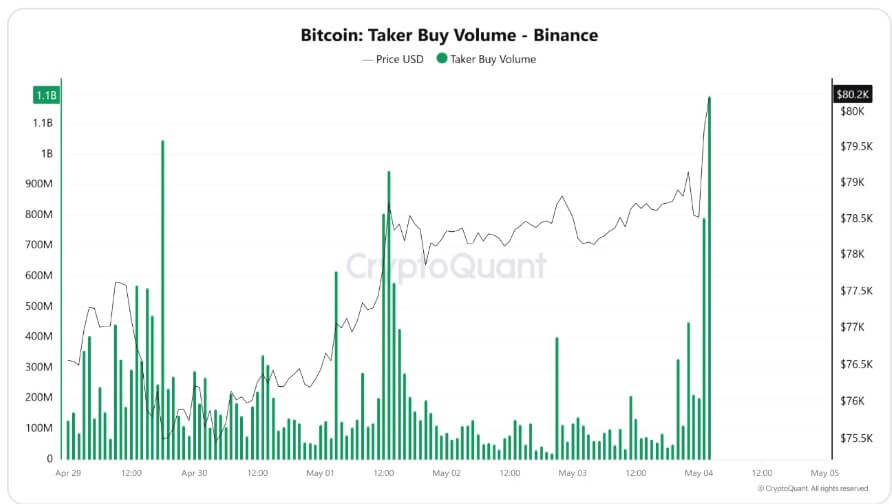

Bitcoin’s initial rise through $80,000 was marked by sheer force rather than organic accumulation.

Facts from CryptoQuant shows that the move focused on major offshore platforms, most notably Binance, where taker-buy volume, a measure that indicates traders exceed the spread to immediately execute at market prices, spiked.

According to CryptoQuant, BTC saw two consecutive increases of approximately $1.19 billion and $792 million on the exchange, resulting in a taker-buy volume of $1.98 billion within a two-hour span.

When this level of aggressive buying manifests itself in a key resistance zone, it typically signals that momentum traders are not waiting for a conservative pullback. Instead, they are actively looking for confirmation of an outbreak.

However, market structure analysts warn that these types of volumes create immediate vulnerability.

CryptoQuant analyst JA Maartunn noted that the asset is now undergoing a real test, highlighting that the price should not remain stuck in this zone for long if the rally is real.

According to Maartunn, Bitcoin must hold above $79,000 at close to maintain structural strength. If the price loses that level, he argues, the weekend’s rise was likely just a liquidity grab to weed out late short sellers.

Derivatives stimulate this movement, but reveal a structural difference

The derivatives landscape further complicates the story, revealing a market struggling with a profound difference between spot psychology and leveraged positioning.

While call options that target upside strikes are heavily populated facts from Deribit, showing $1.7 billion in notional value tied up in the $80,000 call option, alongside huge clusters at $90,000 and $100,000 – the underlying sentiment metrics paint a picture of growing unease.

Instead of a wave of bearish short selling, the market is experiencing a sharp cooling of spot convictions while leverage remains stubbornly long.

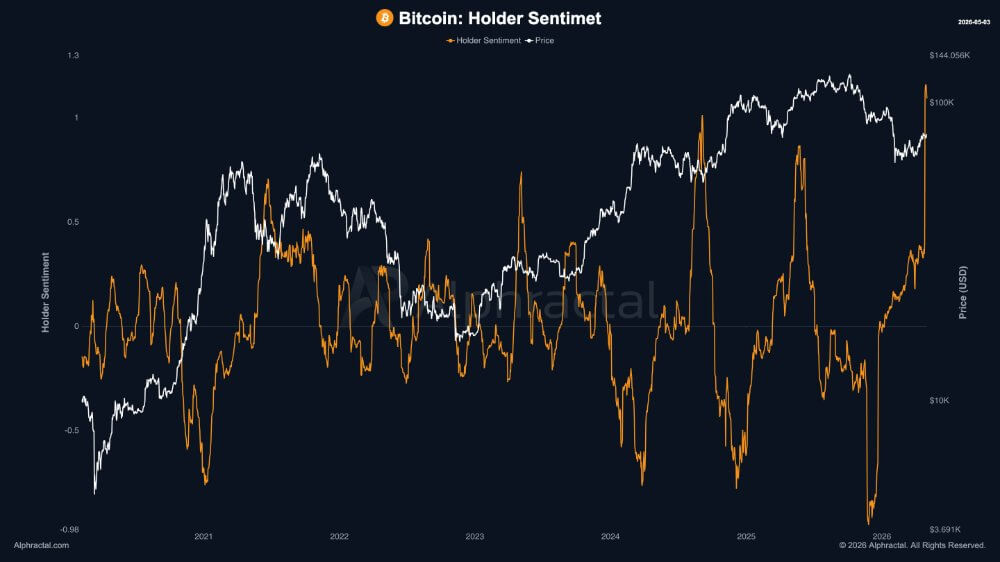

According to data from analytics firm Alphractal, Bitcoin sentiment changed dramatically in less than a week, with the Fear & Greed index falling 10 points to a “Fear” level of 43.

But despite this mock-driven fear, futures traders refuse to back down. Alpharactal data shows that perpetual futures funding rates have remained decidedly positive, currently at +0.51%. This indicates that even though holder sentiment has cooled, speculative traders are still paying a premium to maintain their bullish bets.

This dynamic of fear in the spot market, coupled with long-biased leverage, is critical to understanding current price movements. Historically, this particular difference marks a volatile ‘stress phase’ for the asset.

Consequently, the short push past $80,000 appears to have been driven largely by leverage-sensitive traders, rather than a clean, fundamental macro reset.

As the market continues to rise, this heavy reliance on derivatives makes the structure top-heavy and highly vulnerable to violent long-term liquidations if the macroeconomic situation suddenly sours.

Demand for ETFs points to sustainable spot bidding

While derivatives provide the volatile volatility, US spot ETFs provide the structural floor for the best cryptocurrencies.

Data from SoSoValue shows that US-listed spot Bitcoin ETFs have now recorded two consecutive months of net inflows, totaling $3.29 billion in investor funds. This comes after the outflow that dominated the previous four months.

Notably, this is the first consecutive month of inflows since September and October last year, when the funds raised nearly $7 billion in fresh capital.

Ecoinometrics, a Bitcoin economics platform, explained that current numbers show that “the demand [for BTC] is starting to take hold.” The further declared:

“In recent weeks, Bitcoin ETFs have experienced net inflows for nine days. That’s the longest period of consistent demand we’ve seen in this entire bear market. The last time flows looked like this was in October 2025, right when Bitcoin hit its all-time high. Then demand disappeared and the market rolled over. What’s different now is not the size of the inflows, but their persistence.”

Given the above, this volatility quietly transforms the underlying architecture of the market as real spot demand gradually absorbs the volatility generated by the futures market.

Additionally, CryptoQuant data pointed out that the average cost basis of early institutional ETF buyers now acts as a formidable technical support level for the top cryptocurrencies.

Macro risks shadow the recovery

Despite the crypto market’s improving microstructure, broader macroeconomic realities argue against unbridled conviction.

The geopolitical situation in the Middle East remains tense. Although a ceasefire has temporarily halted hostilities, underlying tensions are actively shaping global risk appetite.

Iran recently issued stern warnings to US forces to stay away from the Strait of Hormuz, a crucial global shipping artery, even after President Donald Trump said the US would intervene to help stranded commercial ships.

This geopolitical friction has kept oil prices well above the $100 per barrel mark, which in turn poses a huge headwind to global disinflation efforts.

Meanwhile, the persistence of energy-driven inflation is forcing a rapid recalculation of US monetary policy.

Instead of taking an easing course, the Federal Reserve is facing pressure to completely abandon its easing bias. As a result, major financial institutions are adjusting their models accordingly; Barclays recently shifted The expectation is that interest rates will be zero for the whole of 2026.

This uncertainty is exacerbated by an impending shift in central bank leadership. Chairman Jerome Powell’s term expires May 15, and his designated successor, Kevin Warsh, has approved the commission. A full Senate vote is expected the week of May 11.

Warsh’s rise introduces a new variable in the pricing of risky assets, as institutional managers hesitate to deploy massive capital without knowing exactly how the new chairman will navigate the tension between persistent inflation and an increasingly taxed economy.