Bitcoin’s aggressive break below $70,000 has shifted the market from a dip-buying debate to a more defensive question about how far traders should now insure against the next move lower.

Data from CryptoSlate showed the largest cryptocurrency falling to $65,404 in the past day, triggering $1.8 billion in liquidations and wiping out the bullish leverage built around hopes for a quick recovery.

This failed recovery has pushed traders toward protection at levels that only recently seemed far away.

Options positioning now shows demand increasing around the $60,000 and $50,000 strikes, a sign that investors are preparing for a deeper reset as Strategy’s first Bitcoin sale in years, ETF outflows, AI-driven capital rotation and unresolved macro pressures weaken the sources of support that carried the market earlier this year.

How BTC’s failed rebound turned $70,000 into resistance

Analysts at BIT Official noted that Bitcoin was already trading defensively after falling to $72,000 last week as geopolitical tensions around the Strait of Hormuz prompted a broad withdrawal from risk assets.

The firm noted that there was a brief reprieve after President Donald Trump suggested the US would lift a naval blockade, while core PCE inflation was in line with expectations at 3.3% annualized in April.

This data and political development eased immediate macroeconomic concerns and forced over-indebted bears to cover their short positions.

As a result, Bitcoin briefly spiked towards $73,400 this weekend, giving bulls leverage to claim the sell-off had been exhausted.

However, that narrative collapsed when the recovery failed to attract meaningful spot volume.

When Iran’s Foreign Ministry explicitly denied nuclear talks, disputed Trump’s uranium claims and insisted the strait would reopen strictly on its own timeline, the geopolitical aid trade disappeared. Without a formal de-escalation, Bitcoin was left completely exposed.

As a result, the market quickly pulled back to $70,000, marking a pivotal moment when options positioning, market psychology, and short-term holders’ cost bases converged.

That level had served as both a psychological bottom for bulls and a prime target for bears hunting for liquidations.

Once Bitcoin cut through that support, automated liquidation engines began aggressively unwinding collateral long positions.

The decline further accelerated rapidly and entered a vacuum as spot buyers proved unwilling to absorb the selling pressure.

Selling strategy gives bears a cleaner script

BTC’s drop below $70,000 also came at a very vulnerable time, as the corporate bond story fell apart.

This week, Strategy confirmed that it sold 32 BTC for $2.5 million to fund cash distributions and dividend payments on its high-yield perpetual preferred stock.

The sale came as a shock to the market as Strategy had positioned itself as the definitive corporate representative for Bitcoin accumulation trading.

In recent years, the Michael Saylor-led business model has relied heavily on equity issuance, preferred stock and unfettered access to capital markets to build the largest publicly traded Bitcoin treasury in existence.

For the broader market, the company was not only a major asset, but also a symbol of permanent, price-independent demand.

However, that perception is now under immense pressure as the company most synonymous with the “never sell” philosophy liquidated coins to meet a routine cash obligation.

Jeff Dorman, Arca’s CIO, noted:

“From a sentiment perspective, how do you think the average Bitcoin investor will react when every major news outlet and social media influencer starts writing that “MicroStrategy is now a seller of BTC”? This company has purchased over $50 billion worth of Bitcoin and currently owns about 4% of the total 21 million outstanding.”

That pivot weaponized a clear, simple argument as Bitcoin slipped below major support.

Market observers argued that the sale complicates the market’s basic assumption that Strategy will act as a continuous buyer in all macroeconomic environments.

Some have even postulated that the company could increase sales in the future to actively manage its balance sheet.

AI’s liquidity attraction means Bitcoin no longer has an ETF cushion

This structural shift in sentiment coincides with the disappearance of Bitcoin’s most reliable safety net: the institutional ETF offering that anchored the earlier phases of the bull run.

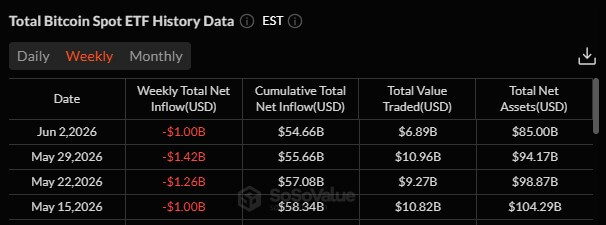

According to data from SoSoValue, Bitcoin ETFs have lost more than $4 billion in the past four weeks. This marks the most aggressive redemption cycle since spot products came to market, starving the market of the steady inflows needed to meet routine sell-offs.

Market analysts attribute this severe capital flight to a generational shift toward artificial intelligence.

Institutional allocators are actively liquidating crypto holdings to clear dry powder for a looming wave of tech mega-IPOs, mainly targeting fast-growing companies like SpaceX, Anthropic and OpenAI.

Pierre Rochard, CEO of the Bitcoin Bond Company, pointed out that this AI boom has added $19 trillion in market cap to the top 50 public stocks over the past twelve months, about 13 times Bitcoin’s total market value.

He said the investment cycle is diverting liquidity and attention from Bitcoin, making the asset’s resilience despite pressure remarkable.

Independent Bitcoin analyst Matthew Case described the move as an “AI IPO liquidity vacuum,” arguing that institutions that pushed Bitcoin and crypto exposure higher now have a rare opportunity to position themselves for large private market and pre-IPO opportunities tied to SpaceX, Anthropic and OpenAI.

This capital rotation is aggressively robbing Bitcoin of its marginal buyer. During periods of robust ETF inflows, institutional demand acts as a shock absorber, cushioning the blow from macroeconomic friction, geopolitical headlines and derivatives volatility.

With that bid suddenly sidelined, the market becomes dangerously exposed; a standard technical decline can continue much further before there is strong support on the ground.

$60,000 will be the next level of insurance in the market

As a result, traders have fundamentally rethought their risk models. The market is no longer structured around highly leveraged bets anticipating a quick return to $70,000.

Instead, capital is aggressively repositioning itself due to the reality that Bitcoin’s next sustainable line of defense could be significantly lower.

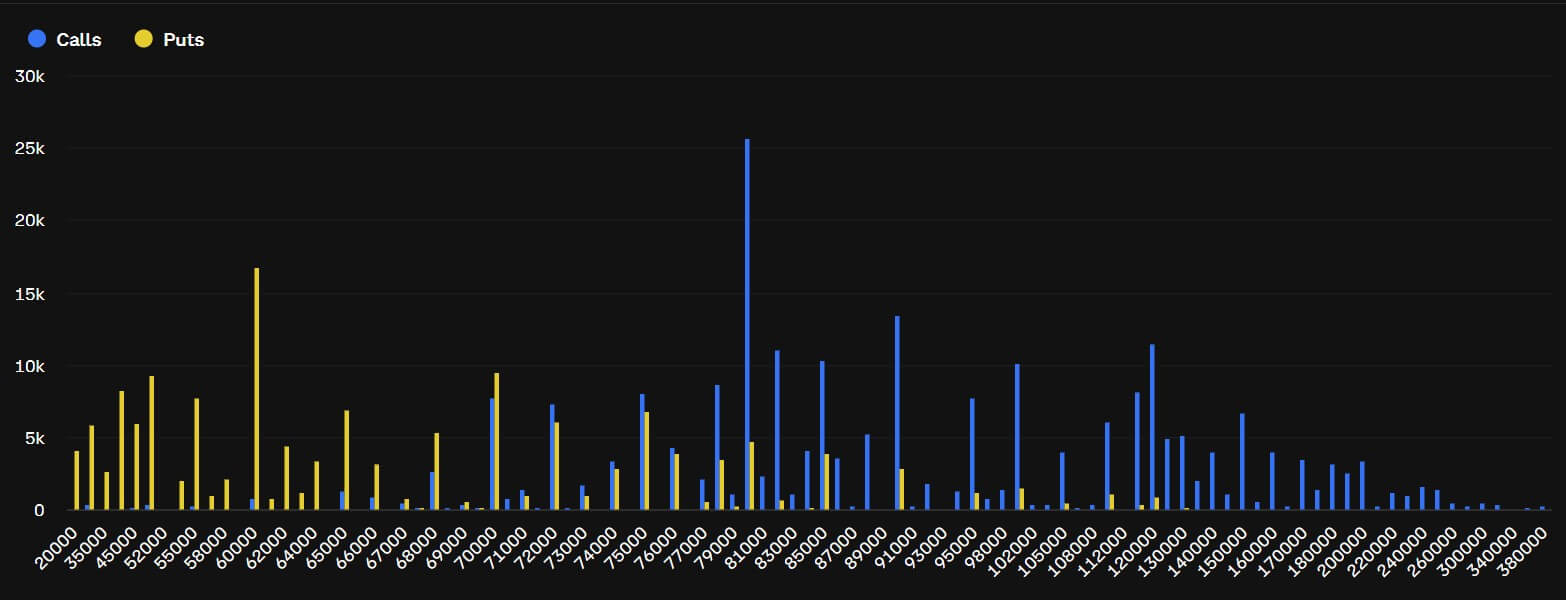

Deribit facts shows that traders have accrued about $1.2 billion in open interest around the $60,000 strike, while the $50,000 strike has generated about half that amount. Cumulatively, there is $1.8 billion in open interest at these strike prices.

The positioning marks a change from the structure that dominated the rally earlier. When ETF inflows were strong and Strategy remained an uncontested buyer, pullbacks were seen as opportunities to increase exposure.

Following the wave of liquidations, ETF redemptions and Strategy sales, the same withdrawals are treated as insured events.

As a result, traders with significant exposure to Bitcoin are moving toward put and collar structures designed to preserve some upside potential while limiting losses if the decline accelerates.