For traditional US banks, the CLARITY Act was intended as a firewall that effectively bans crypto companies from offering “passive” interest on stablecoins.

The legislation was intended to prevent catastrophic deposit flight, where daily checking account balances flow out of the banking system and into high-yield crypto exchanges.

But as lawmakers prepare to finalize the framework, Coinbase appears to be quietly structuring a loophole that relies on complex financial engineering to keep the lucrative returns flowing.

The key lies in a critical semantic distinction within Section 404 of the proposed legislation. While the CLARITY Act explicitly prohibits interest on savings accounts on stablecoins, activity-based rewards will remain.

Enter Ethena, a synthetic dollar protocol that generates returns via active, delta-neutral basis trading that involves shorting perpetual crypto futures while holding the spot assets.

By integrating with Ethena, Coinbase could theoretically incorporate inactive USDC into this strategy.

If successful, the exchange could pass on the profits of an active trading strategy and potentially offer huge returns on digital dollars right under the noses of regulators, while the traditional banking sector would be seriously frustrated if stuck offering negligible rates.

The legislative wall called CLARITY Act

The CLARITY Act, a sweeping US market structure law designed to define how crypto assets and intermediaries operate under federal regulations, has been a legislative battleground.

At the center of the dispute that has delayed the Senate Banking Committee process is the issue of stablecoin rewards.

The latest compromise is primarily enshrined in Article 404, which emerged from the Tillis-Alsobrooks amendment. The provision draws a hard regulatory line that the industry has negotiated for months.

On the one hand, there is passive return: simply holding a stablecoin balance and receiving periodic interest, which is structurally identical to a bank savings account. This is explicitly prohibited.

On the other hand, there are activity-based rewards: incentives related to actual customer activity, such as payments, transactions, platform usage and commerce. These are allowed.

The banking lobby pushed hard for these restrictions. Bank executives believe that companies offering bank-like products should face similar supervisory, reserve and capital requirements.

If crypto platforms could freely pay savings account interest on stablecoin balances without FDIC insurance requirements, they could easily siphon depositors’ capital at the expense of the regulated banking system.

JPMorgan Chase CEO Jamie Dimon recently expressed this exact frustration. In a recent one interviewDimon criticized Coinbase CEO Brian Armstrong, warning that the CLARITY Act could fail if traditional banking problems are not addressed.

When asked if he was satisfied with the current bill, Dimon replied bluntly:

“No, because it allows them to effectively pay interest on deposits, stablecoins or the like, without the protections they should have. The banks won’t accept it that way…”

For the legislation to become law, representatives from the Senate Banking and Agriculture committees must put together their advanced bills before it passes the full Senate and House of Representatives and lands on President Donald Trump’s desk. But while Washington debates, the crypto industry is already building around the new rules.

Coinbase’s Ethena solution

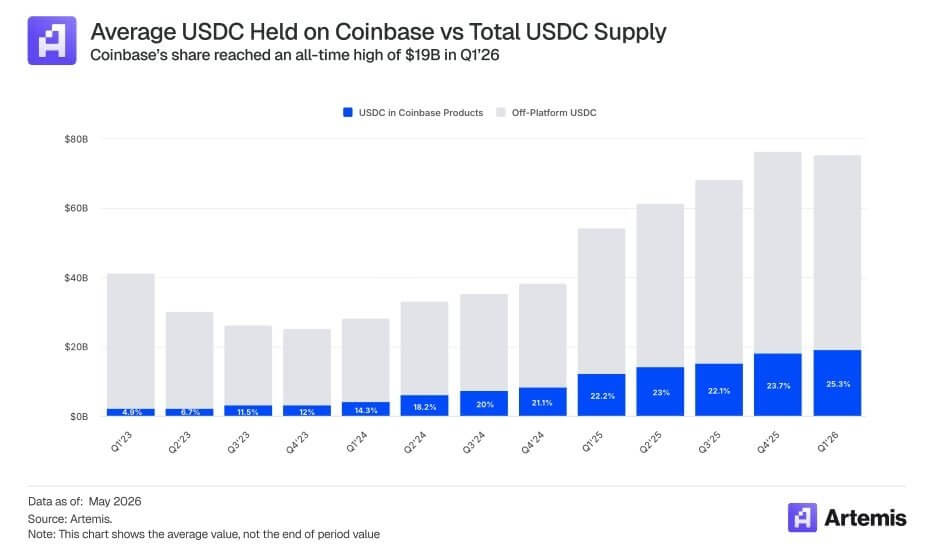

Coinbase relies heavily on stablecoins. In the first quarter of 2026, the exchange reported $305.4 million in stablecoin revenue, accounting for approximately 52% of subscription and service revenue.

The company also stated that it held an average of approximately $19 billion in USDC in its products, accounting for more than 25% of the total USDC in circulation.

To protect this vital revenue engine under Section 404, Coinbase needed a product in which revenue is tied to explicit activity rather than passive ownership. The new collaboration with Ethena ensures a perfect thread for this needle.

Ethena stated:

“Ethena and Coinbase are working together to grow on-chain financing and savings products for their more than 100 million users, with the first growth initiative launching next week.”

In addition to the integration, Coinbase Ventures made its first investment in Ethena on the open market.

Coinbase also confirmed its expanded role, noting that it will support the security and operations of more than $5 billion in Ethena assets. Coinbase now serves as Ethena’s primary custodian, wallet provider, and perpetuals location.

Because Ethena generates returns through complex trading activities, Coinbase can redirect yield-oriented USDC users to real loan demand and active market strategies.

Guy Young, the founder of Ethena, explicitly acknowledged the regulatory tailwind, proverb:

“Excited to partner with Coinbase for the first time to support their dollar savings products…Given the evolving nature of the Clarity Act, we expect further potential tailwinds for onchain native products such as USDe from inactive balances on exchanges, and Ethena is well positioned to support this transition.”

Yan Liberman, managing partner at Delphi Ventures, highlighted exactly how lucrative this structural shift could be for both parties. He declared:

“Between the lines for the upcoming product launch is being referenced. Coinbase x Ethena is bullish because it can turn Coinbase’s ~19 billion USDC base, with an implied ~13 billion USD in reward balances, into a funding track for Ethena. If sUSDe delivers clear base USDC rates, Coinbase can offer better USDC loan yields, loopers can leverage the spread, and Ethena gets deeper/cheaper funding than just it native DeFi. Aave mechanics, Coinbase distribution.”

Liberman added that the CLARITY Act makes this pivot very valuable. If lawmakers limit passive USDC rewards, Ethena gives Coinbase a way to direct users to real lending demand instead of simply paying them for holding USDC.

He added:

“Coinbase needs products where returns are tied to explicit activities: lending, collateral, liquidity, or platform usage. Ethena gives them a way to direct yield-oriented USDC users to real loan demand, rather than just paying rewards for holding USDC.”

The new ‘Coinbase problem’ for banks

While banks may feel protected by Section 404’s ban on passive interest, Ethena’s loophole poses a new and immediate threat.

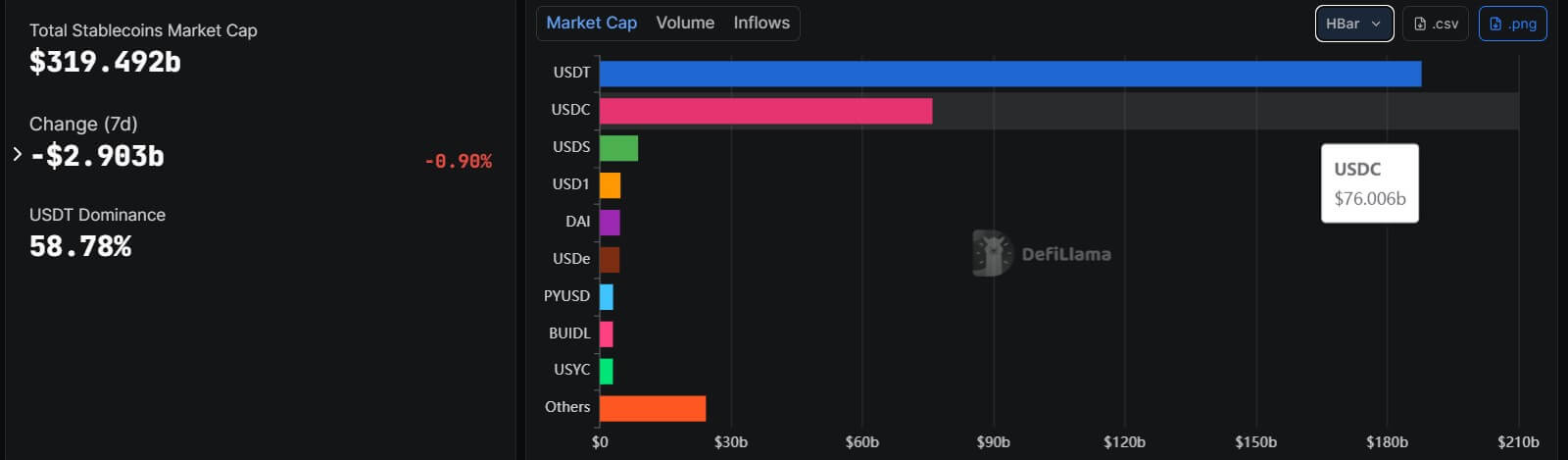

Stablecoins have outgrown their origins as a niche settlement layer. The total stablecoin market is roughly $320 billion, with USDC being around $76 billion and Ethena’s USDe being around $4.5 billion.

Because Circle backs USDC with highly liquid cash and cash equivalent assets with monthly attestations, Coinbase’s strategy uses USDC as the trusted settlement asset, while Ethena provides the yield-bearing synthetic dollar layer.

Granted, an immediate systemic bank run is unlikely. American commercial bank deposits was roughly $19.3 trillion at the end of May 2026, and money market fund assets were $7.78 trillion. Even if Coinbase were to convert its entire USDC balance of $19 billion, this would be a drop in the bucket compared to the broader banking system.

However, the real danger for the banks is the marginal price pressure.

When mobile, yield-sensitive retail clients and institutional treasuries realize they can seamlessly access ~3.8% APY through an activity-based Ethena strategy in a Coinbase app, they will inevitably move their idle cash.

To stem the outflow, traditional banks may be forced to raise their own historically low deposit rates, directly affecting their net interest margins. It is striking that American savings accounts yield only 0.38%, while interest accounts reach the bottom at 0.07%.

Additionally, Tom Wan, head of research at Entropy Advisors, says pointed out that the integration of Coinbase and Ethena could be the start of an institutional synergy that bypasses traditional banking entirely.

Wan notes that Ethena can leverage institutional lending through Coinbase Asset Management, use Coinbase Custody, and use USDC as liquid stablecoin backing. In the future, Coinbase could become a primary base trading platform and allocate supporting assets to lending protocols such as Aave on Base to grow USDe as a dominant savings product.