XRP’s latest decline exposes a widening divide between traders betting on more weakness and investors using the sell-off to build exposure.

In recent weeks, the digital asset has faced persistent downward pressure caused by capitulation of short-term holders and aggressive short selling in futures markets.

However, underlying spot market demand has proven resilient, as evidenced by the fact that XRP-linked exchange-traded funds are on track to post their strongest monthly performance of the year.

This market disconnect is playing out as Ripple accelerates its expansion into institutional financing, giving long-term investors a structural adoption story even as momentum traders exit at a loss.

For market participants, the crucial question is whether XRP establishes a macro accumulation base or simply pauses within a long-term downtrend.

Trader losses mount as sentiment sours

Underneath XRP’s sluggish price action lies significant retail turmoil. According to blockchain analytics firm Santiment, the average trader active in the token in the last 30 days has unrealized losses of around 47%.

The decline pushed XRP’s 30-day market value-to-realized value (MVRV) ratio to its lowest point since December 2020.

The steep decline marks a sharp reversal from recent optimism. XRP rose in late 2024 and early 2025 as investors factored in favorable regulatory developments, the debut of US exchange-traded funds and Ripple’s evolving business profile.

The subsequent pushback trapped many latecomers, leaving them underwater after gaining ownership near local peaks.

In cryptocurrency markets, deeply negative MVRV values often serve as a gauge of trader exhaustion rather than a direct directional signal.

When a large part of the short-term holding base is seriously compromised, the risk of forced selling generally decreases. For XRP proponents, this zone suggests that months of liquidations may be coming to an end.

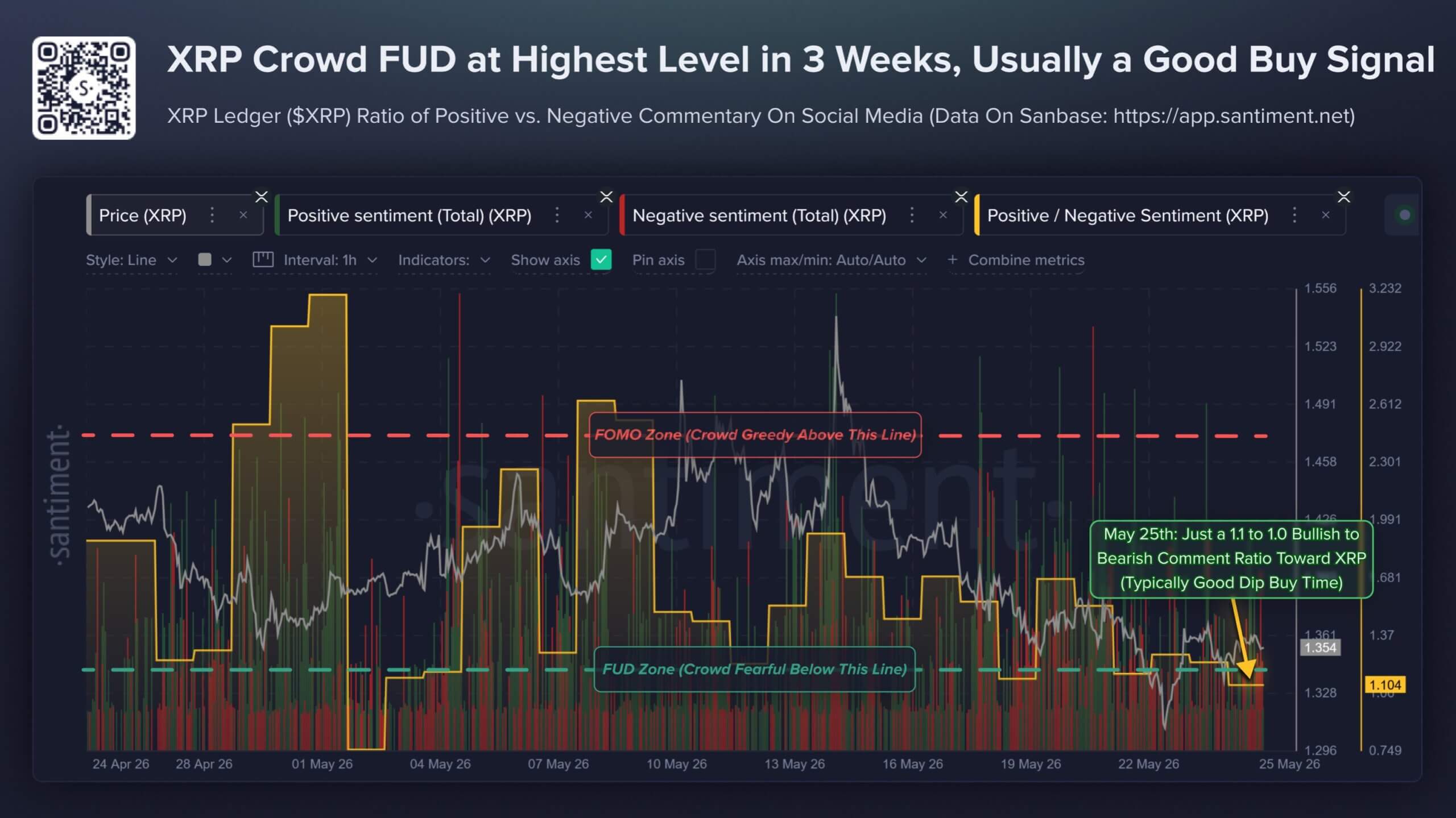

Furthermore, the public’s broader sentiment surrounding the token is consistent with this exhaustion.

Santiment’s positive/negative comment ratio for XRP has compressed to around 1.1 bullish comments for every bearish comment, indicating that the speculative fervor that defined previous rallies has largely evaporated.

While extreme pessimism can serve as a contrarian indicator, indicating that weak hands have exited the market, sentiment alone is insufficient to catalyze a reversal.

Thus, XRP requires clear evidence of buyer belief that can withstand the heavy selling pressure coming from leveraged trading platforms.

The sale of derivatives is accompanied by absorption on the spot market

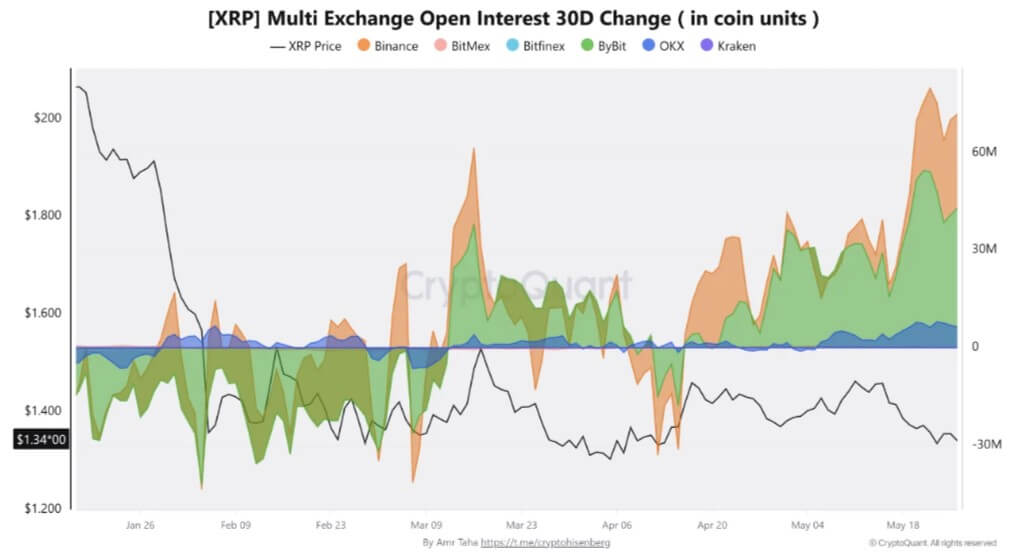

The structural gap between retail capitulation and institutional accumulation is most visible in stock market order books.

Facts compiled by CryptoQuant shows a sharp division between XRP’s spot and derivatives platforms.

On May 22, open interest for XRP expanded aggressively on centralized derivatives exchanges. Binance recorded an addition of approximately 25.6 million XRP in open interest, while Bybit added 54 million XRP.

The combined injection of nearly 79.6 million XRP had a notional value of approximately $107 million, with the assets trading around $1.35.

A subsequent surge occurred on May 26, when Binance’s open interest rose by another 28.9 million XRP, combined with a 42.9 million XRP increase on Bybit. At an average price of $1.34, this represented $96 million in new speculative positioning.

These events marked the most significant expansions in XRP open interest since mid-March, signaling a return of speculative leverage after a two-month lull.

However, the direction of that influence provides the critical context.

Binance’s cumulative volume delta (CVD) perpetual futures has fallen to a record negative figure of approximately -$641.9 million. This metric indicates that aggressive short sellers have dominated the perpetual market and have continuously bet on the token even as open interest rises.

Conversely, spot markets show the opposite trend. The estimated spot CVD across all centralized exchanges has increased to approximately $397.3 million, surpassing the $380 million threshold set at the end of April.

The difference is stark: traders make heavy use of leverage to short XRP, while spot buyers consistently take the other side of these trades.

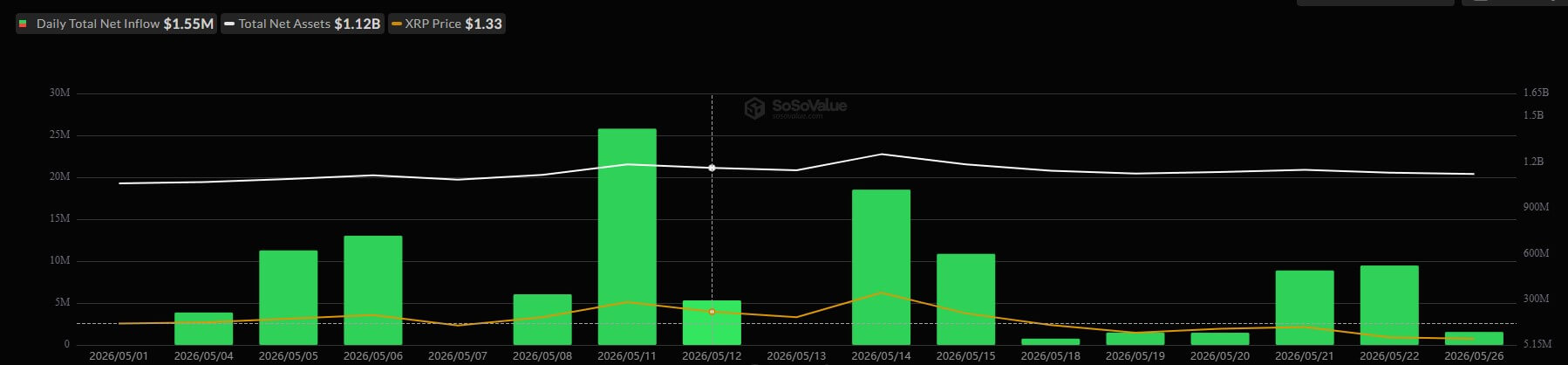

The XRP-linked ETF products confirm this absorption thesis. Data from SoSoValue shows that US-listed XRP spot funds are on track for their strongest monthly performance this year, attracting around $117 million in recent inflows and extending their positive streak to 13 consecutive trading sessions. This has pushed their cumulative inflows above $1.12 billion.

While ETF inflows cannot fully offset pressure on the futures market, they provide a regulated anchor for the asset.

The data suggests that XRP’s current price weakness is being absorbed by capital with a longer investment horizon, shifting the market focus to Ripple’s business developments.

Ripple’s Wall Street raid strengthens the fundamental case

Ripple’s continued strategic pivot has injected a new fundamental story into the XRP market structure.

The company recently submitted US trademark applications that reflect a clear ambition to integrate traditional financial activities, including treasury activities, prime brokerage, hedge fund management, securities lending, financial clearinghouse services and digital asset management.

While trademark applications do not guarantee the launch of specific products, they do define a company’s strategic perimeter. In this case, the documents indicate a calculated strain on the core infrastructure of institutional finance.

This direction is consistent with the company’s continued aggressive business building that began last year.

During this period, Ripple structured a vertically integrated business consisting of Ripple Prime, which serves as an institutional trading desk; Ripple Custody, which safeguards assets through institutional-grade architecture; and Ripple Payments, which functions as a cross-border settlement layer.

XRP and the RLUSD stablecoin act as the connective tissue, facilitating the liquidity and treasury workflows in these divisions.

Market observers noted that Ripple is positioning itself as a crypto-native alternative to traditional clearinghouses and investment banks by going beyond its original mandate of cross-border money transfers.

This evolution offers long-term XRP holders an adoption thesis separate from retail enthusiasm.

What’s next for XRP?

As Ripple builds its institutional framework, on-chain data is fueling debate about the macro trajectory of the XRP Ledger (XRPL).

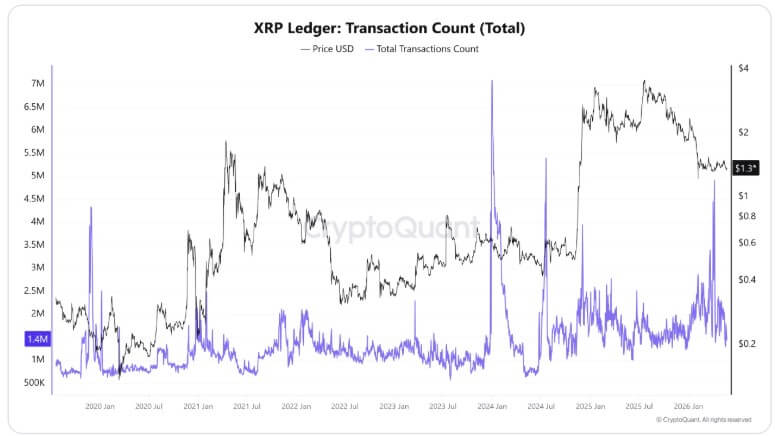

Additional facts from CryptoQuant highlight massive, abnormal spikes in the number of XRPL transactions. Historically, these vertical increases in network activity have served as leading indicators, occurring months before significant price increases.

In November 2019, an extreme spike in trading volume preceded XRP’s 2021 bull run, with the token rising from around 15 cents to $1.79. A parallel event occurred in July 2024, acting as a precursor to the 50-cent asset’s climb to the cycle peak of $3.17 in mid-2025.

Market analysts are now exploring a similar explosion in transaction volume, recorded in April 2026. Following this surge, XRP has entered a prolonged consolidation phase, trading mainly within the $1.30 to $1.50 range.

Proponents of this cyclical theory argue that if historical patterns hold and the current range solidifies to a macro floor, a standard multiple expansion could position XRP’s next cycle target between $7.50 and $8.00.

However, such projections remain speculative cycle comparisons and not guaranteed predictions. Previous network spikes did not cause an immediate price increase; they were followed by extended periods of reaccumulation, cooling and structural market realignment.

For XRP to achieve a sustained rally toward these goals, the market would need to exhibit continued spot absorption, a capitulation of short sellers in the derivatives market, and a definitive technical breakout.

Currently, the market is still in a state of friction. Retail traders are suffering heavy losses, sentiment is deeply depressed and futures speculators are aggressively shorting assets.

Still, the strengthening of the cumulative volume delta, consistent ETF inflows, and Ripple’s steady encroachment on Wall Street’s infrastructure suggest a robust counter-narrative.

If spot market demand continues to offset derivatives sales, the current period of extreme pessimism could ultimately be seen as a fundamental accumulation phase.

Until that underlying demand is exhausted or triumphant, Ripple’s institutional expansion remains a forward-looking catalyst anchored in a market awaiting its next decisive move.