A recent American Bankers Association (ABA) ad running through Washington shows a clear lead in a campaign that has been going on for months.

The advertisement reads:

“Protect local lending while embracing innovation. Tell senators to close the stablecoin loophole.”

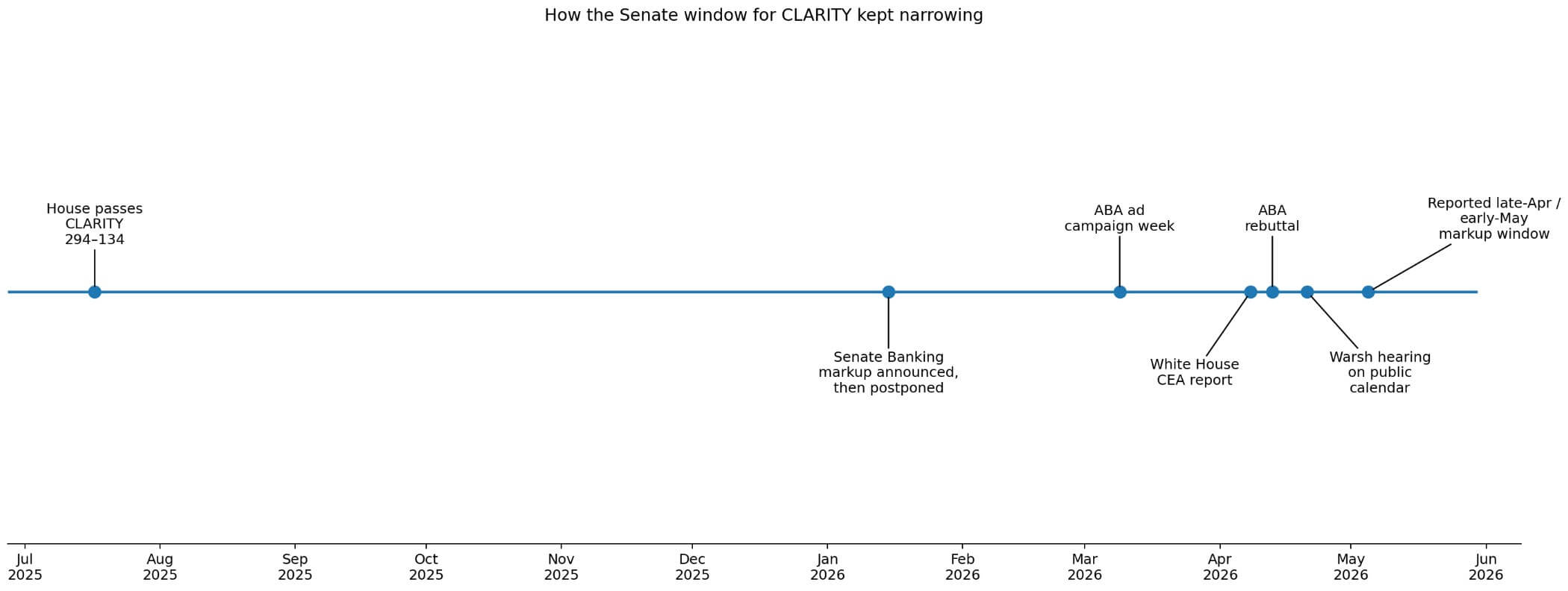

The ABA ad archive documents Politico Morning Money placements the week of March 9, urging senators to take action on stablecoin yields, as well as a separate digital campaign targeting Congress, the White House and regulators.

In January, more than 3,200 bankers signed a letter calling on the Senate to close what they called the “payment of interest loophole.”

ABA-backed trade groups followed with a joint letter asking Congress to codify a comprehensive ban on stablecoin incentives paid by issuers, affiliated platforms, or third-party partners.

The ABA’s Community Bankers Council added that $6.6 trillion in deposits could migrate if the language remains loose. These are advocacy metrics that document how coordinated and sustainable the campaign has been.

It all now ends up on a Senate calendar that has very little space.

The House passed the CLARITY Act on July 17, 2025 by a margin of 294 to 134, more than enough to give the Senate a clear mandate to act. Senate Bench Chairman Tim Scott announced a committee increase for January 15, 2026.

The committee still lists that session as postponed on the official format page, with no replacement date. The committee’s current public schedule includes a hearing for Kevin Warsh’s nomination on April 21, with no mention of CLARITY marking.

Reports indicate a possible increase in the last week of April or the second week of May, and that time before the summer campaign season is limited, and that the bill still raises unresolved disputes over ethical and illegal financing provisions that go beyond the battle between the banks.

Each additional round of negotiations over stablecoin yields further narrows the window. Keeping the interest rate battle alive long enough to compress the timeline is itself a victory for the banking lobby.

What the battle is actually about

The GENIUS Act already prohibits stablecoin issuers from directly paying interest or returns. The banking lobby is targeting the current draft language because it does not explicitly prohibit affiliated platforms or third-party partners from paying rewards in tokens.

A crypto exchange that owns a yield-bearing stablecoin could effectively compete for deposits under that architecture. Banks want that channel to be closed. That is the meaning behind the word ‘loophole’.

The White House Council of Economic Advisers (CEA) concluded that banning returns on stablecoins would increase bank lending by only $2.1 billion, or 0.02% of the current base, with a net welfare cost of $800 million.

Big banks would account for 76% of the added lending, while 24% would go to community banks, the constituency at the center of the local lending debate.

ABA said five days later that CEA had studied the wrong question, arguing that the real exposure is a future scenario in which yield-bearing stablecoins are large enough to compete directly with deposits, taking funding out of the banking system before regulators can respond.

The two sides are debating the size of the stablecoin market under different assumptions, and senators must now resolve this dispute.

| Actor | Main claim | Key number/proof | What they want |

|---|---|---|---|

| ABA / banking groups | A loose revenue language could let stablecoins compete with deposits through affiliates and partners | 3,200+ bankers signed letter from January; advocacy estimate of $6.6 tons in potential depositional migration | Close publisher, partner, and third-party rewards channels |

| White House CEA | An interest rate ban has only a modest effect on bank lending in the short term | $2.1 billion added loans, 0.02% from base, $800 million welfare costs; 76% of the additional lending goes to large banks | Avoid exaggerating the current credit benefits of prohibition |

| BIS / Pablo Hernández de Cos | Deposit shifts could be smaller if stablecoins remain unremunerated and interest rate bans are enforceable | Supports the importance of reward rules in larger scale scenarios | Maintain an enforceable non-yield design as stablecoins scale |

| Senate negotiators | Language is needed that addresses the “loophole” without derailing CLARITY | The public agenda does not yet show any markers; the timing pressure increases | Reach a compromise quickly enough to maintain momentum |

BIS chief Pablo Hernandez de Cos said on April 18 that deposit shifts could be smaller if stablecoins remain unfunded and interest rate bans can be enforced, a direct validation of the scale-dependent logic ABA has been running.

The White House analysis and the BIS warning are consistent in recognizing that, in a worst-case scenario, a rate ban could ultimately generate $531 billion in additional aggregate lending.

Washington is now writing rules for a market that may later be significantly larger.

The coordinated campaign

The public-private combination on the banking side makes this moment different from previous rounds of crypto lobbying. The ads create visible congressional heat, while the bankers’ letters give members an argument about the size of their constitution.

The CEO-level calls establish executive accountability, and ABA’s active rebuttal of the White House report confirms that the lobby is directly challenging the economy, in quantitative terms.

That combination puts CLARITY’s Senate timeline in jeopardy. The bill has the support of the White House, a strong vote in the House and broad support from the industry.

Resolving the committee scheduling problem will require agreement on the terms before the calendar forces a recess or conflicts with Warsh’s confirmation process. Without that, the delayed January markup becomes a pattern.

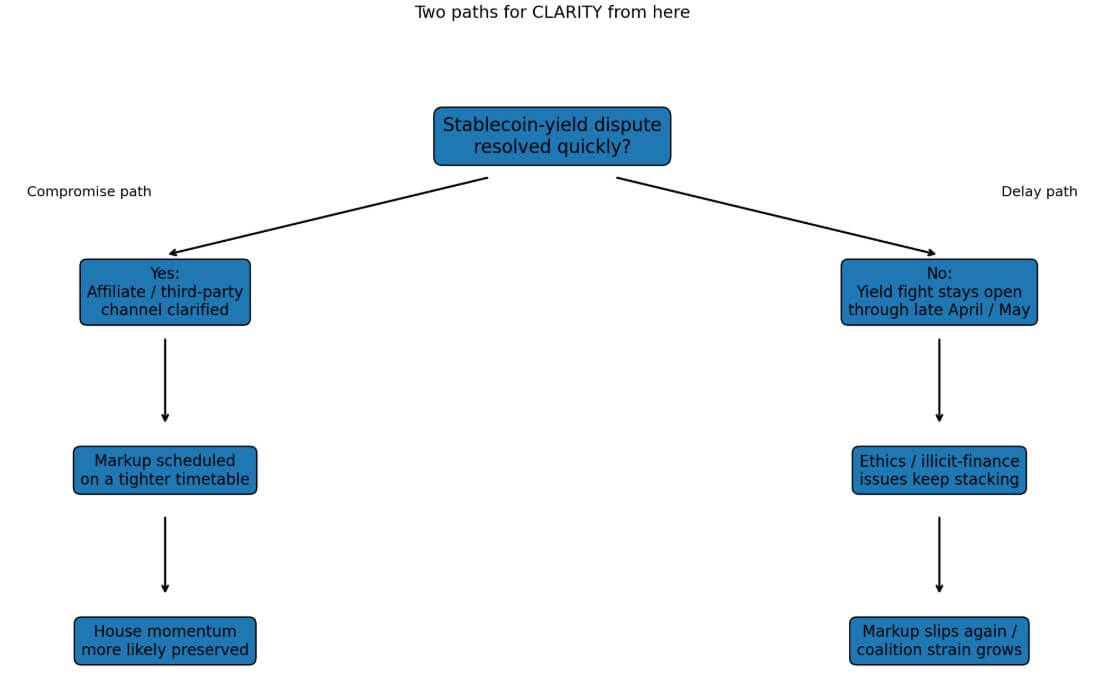

The two paths ahead

The constructive path is through a yield compromise that closes off affiliate and third-party channels clearly enough to at least satisfy the community bank argument, while retaining enough flexibility to keep stablecoin-adjacent products viable.

The White House report gives negotiators a quantitative basis to hold the line, as the U.S. credit benefit from a comprehensive ban in the near term is documented and modest.

Senators Thom Tillis and Angela Alsobrooks are among the most visible members addressing the stablecoin language. If either comes up with a limited compromise that addresses the affiliate channel dispute, an increase could happen quickly enough to maintain whatever momentum the vote still has in the House of Representatives.

Language must close the affiliate channel clearly enough to remove ABA’s loophole argument and flexible enough to keep Circle, Coinbase, and their allies at the table.

Extending that logic to affiliates and platforms faces an obstacle of political will.

The more difficult path is already visible on the Senate’s public agenda. If banks conclude that maintaining the current position provides better long-term conditions than accepting a partial profit, the battle over rates will continue through May.

The disagreements over ethics and illegal financing cause CLARITY to arrive at a markup with more than one open question. Multiple unresolved provisions in a compressed calendar lead to a failure of coalition management, and they go deeper than any planning solution can address.

The ABA ad confirms that the association still views the stablecoin section as unfinished business and is willing to spend public campaign capital to say so.

Combined with a committee homepage showing a Warsh hearing and a delayed layout page still showing the January date, the ad falls within a documented record of coordinated lobbying, active economic struggle and a Senate calendar with no announced path forward.

The bank lobby’s escalation, the White House’s quantitative rebuttal, and the Senate’s public silence on a new markup date all point to the same variable indicating that language must close within days for CLARITY to hit the markup before the campaign season consumes the floor schedule.