Bitcoin’s early 2026 rebound has pushed back into a known problem area: a dense supply of overhead that has repeatedly capped rallies since November, according to Glassnode. In its latest Week On-chain report, the analytics firm describes the move above $96,000 as constructive on the surface, but still largely dependent on derivatives positioning and liquidity conditions rather than continued spot accumulation.

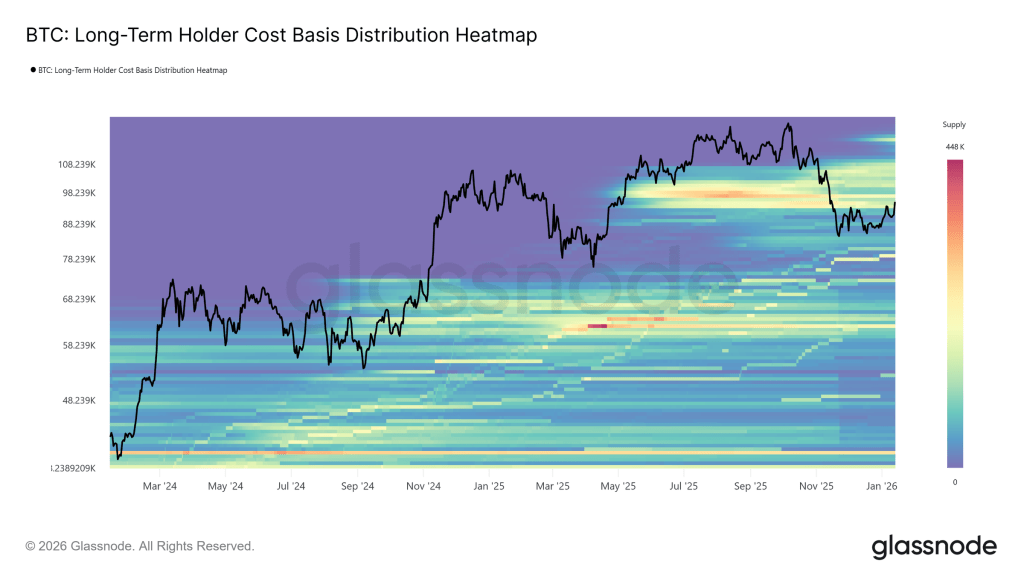

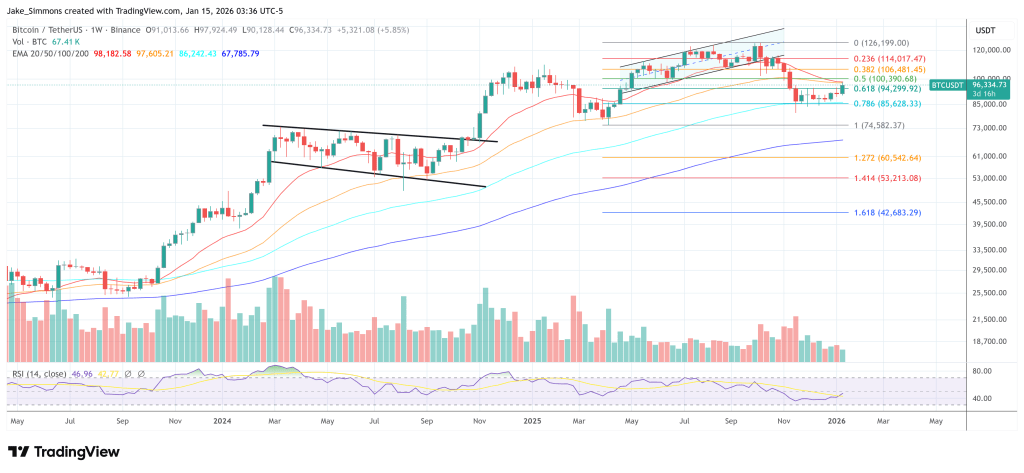

Glassnode is central argument is that Bitcoin has moved directly into a historically significant long-term cost basis (LTH) range, built between April and July 2025 and associated with sustainable distribution near cycle highs. The report describes a “dense cluster” spanning roughly $93,000 to $110,000, with the rebound repeatedly stalling near the lower bound since November.

“This region has consistently functioned as a transition barrier, separating corrective phases from sustainable bull regimes,” Glassnode wrote. “With price once again putting pressure on this overhead supply, the market now faces a familiar test of resilience, with long-term distribution absorption remaining a prerequisite for a broader trend reversal.” The company’s formulation is blunt: the market is back at the same sales ceiling, and achieving this will require real absorption, not just price research.

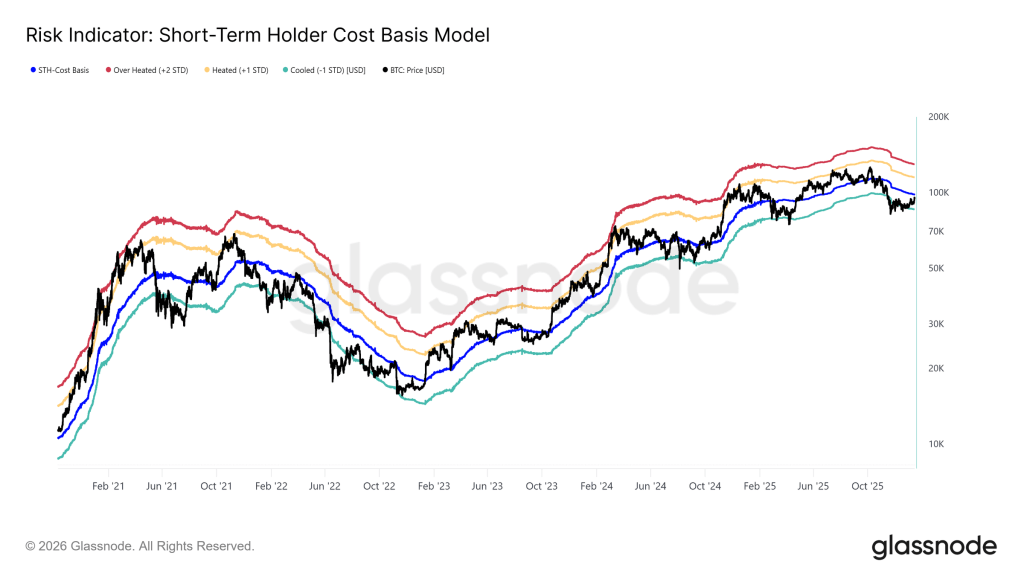

The next level highlighted in the report is the short-term holder cost basis (STH) of $98.3K, which is considered a confidence gauge for newer buyers. Sustained trading above would indicate that recent demand is strong enough to allow latecomers to make profits while sucking up overhead supply.

On-chain, Glassnode notes that long-term holders remain net sellers, while overall LTH supply is still lower. The most important change is speed. The report says the pace of decline has “slowed significantly” from the aggressive distribution seen in the third and fourth quarters of 2025, suggesting profit-taking continues, but with less intensity.

Related reading

“What follows will depend primarily on the ability of the demand side to absorb this supply, especially from the investors gathered in the second quarter of 2025,” the report said. “If it does not remain above the true market average of ~$81,000 over the long term, the risk of a deeper capitulation phase would increase significantly, reminiscent of the period from April 2022 to April 2023.” It’s one of the clearest downside conditions in the note: If the market loses the long-term average, the probability distribution shifts toward a more severe recovery.

A related signal is long-term holders’ net realized gains and losses, which Glassnode says reflect a “significantly cooler distribution regime.” Long-term holders realize a net profit of approximately 12.8k BTC per week, a sharp slowdown from cycle peaks above 100,000 BTC per week. This moderation does not mean that the capitulation risk has disappeared, but it does suggest that the heaviest phase of profit-taking has diminished.

Demand for Bitcoin remains uneven

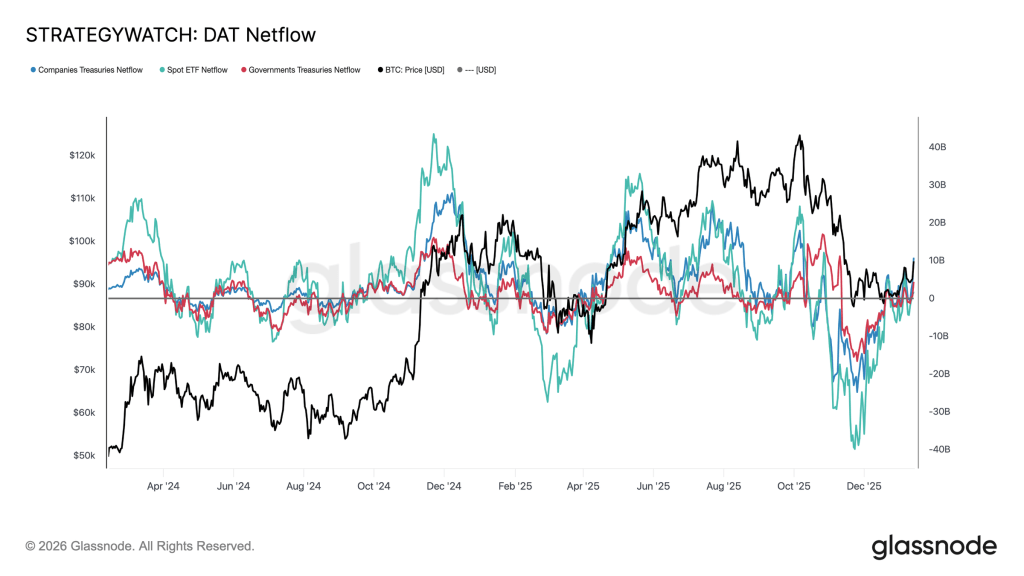

Indicators outside the chain are more constructive. Glassnode argues that institutional balance sheet flows have “undergone a complete reset” after months of heavy outflows from spot ETFs, corporates and sovereign entities, with net flows stabilizing as sell-side pressure appears exhausted. Spot ETFs are described as the first cohort to turn positive again and reposition themselves as the main marginal buyer.

In contrast, cash flows from corporate and government bonds are depicted as sporadic and event-driven rather than consistent. The result is a market where balance sheet demand can help stabilize prices but may not yet function as a sustainable growth engine, making prices more sensitive to derivative positioning and liquidity conditions in the short term.

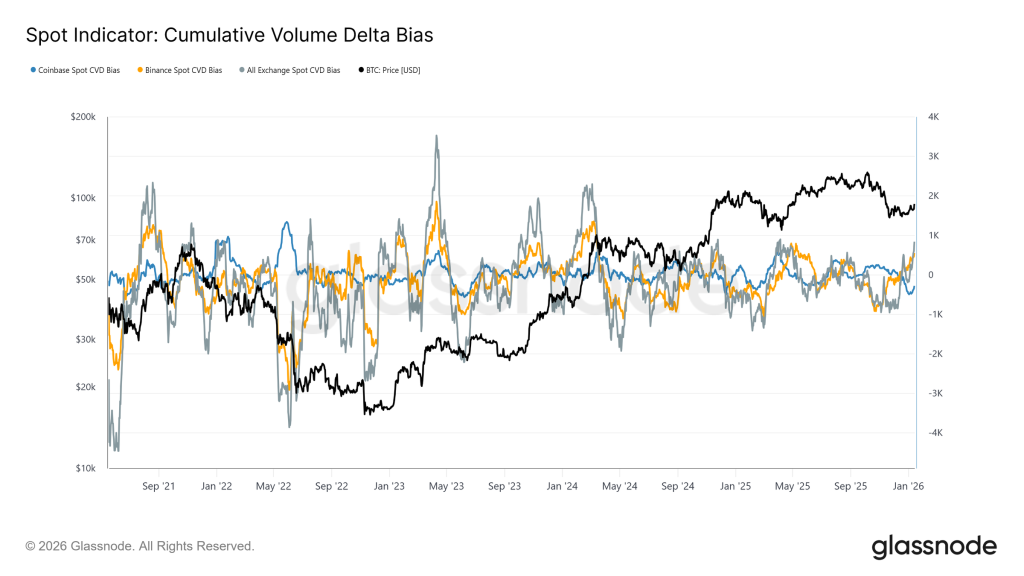

At a location level, Glassnode points to improving spotting behavior. Binance and total exchange rate measures have returned to buy-dominant regimes, and Coinbase, described as a consistent source of sell-side aggression during the consolidation, has “meaningfully slowed its selling activity.” The report calls this a constructive structural shift, but emphasizes that it still falls short of the sustained, aggressive accumulation that typically accompanies full trend expansions.

Related reading

The most vocal warning in the report is that the move into the $96K region was “mechanically amplified” by short liquidations in a relatively lean liquidity environment. Futures turnover remains well below the high activity seen through most of 2025, implying that relatively little capital was needed to force short positions and push prices through resistance.

“This indicates that the breakout occurred in a relatively light liquidity environment, where modest positioning shifts could trigger disproportionately large price reactions,” Glassnode said. “In practical terms, significant new capital was not required to drive shorts out of the market and push the price higher through resistance.” The implication is that continuation now depends on whether spot demand and sustained volume can replace forced coverage once the pressure impulse dissipates.

Options markets add a second layer of tension. Glassnode describes implied volatility as low but ‘delayed’, while skew continues to cause downward asymmetry, with the 25 delta skew biased towards intermediate and longer term puts. In short, participants appear comfortable with holding exposure, but remain unwilling to do so without insurance.

Positioning is also important at the microstructure level. The report flags dealers as short range around the spot, with a zone of roughly $94,000 to $104,000. In that setup, hedging flows can amplify moves rather than dampen them, buying into rallies and selling into dips, increasing the likelihood of accelerating to high-yield price gains like $100,000 if momentum continues.

At the time of writing, BTC was trading at $96,334.

Featured image created with DALL.E, chart from TradingView.com