President Donald Trump’s family has turned crypto into one of the most lucrative businesses tied to his name, surpassing some of the companies that spent years building the digital asset market.

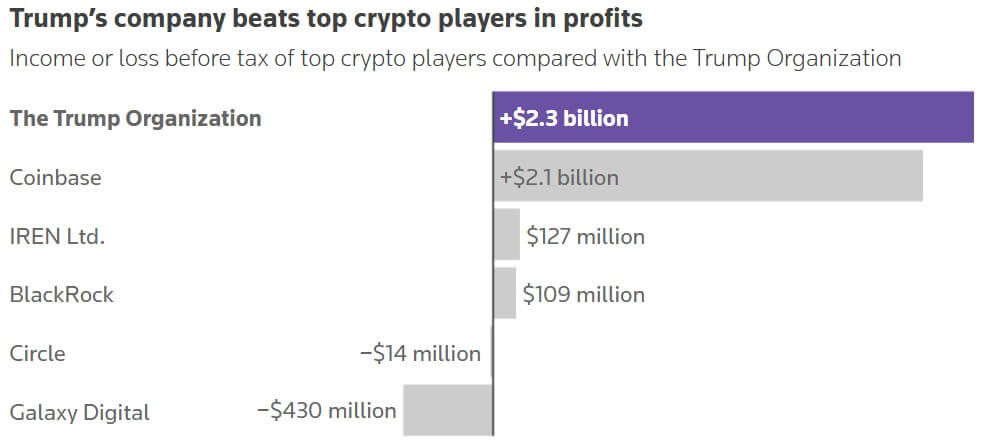

Between the post-election momentum of November 2024 and April 2026, companies linked to the US president generated about $2.3 billion in pre-tax crypto revenue, according to Reuters reported.

To understand the enormity of this capital extraction, one must look at the fundamental pillars of the industry during that same window.

For context, the Trump company’s profits surpassed Coinbase’s revenues over the same period of $2.1 billion, as well as the revenues of major crypto operators in mining, stablecoins, exchange-traded funds and market infrastructure.

IREN, the largest Bitcoin miner by market value, earned $127 million in the period. BlackRock’s Bitcoin ETF business, built around IBIT, the world’s largest spot Bitcoin fund, generated an estimated $109 million.

Meanwhile, Circle, the USDC stablecoin issuer, lost $14 million, while Galaxy Digital, a major crypto company, posted a $430 million loss.

Unlike Coinbase or BlackRock, the Trump Organization did not compete on trading latency, deep liquidity, or assets under management.

Instead, it used a very different business model: an asymmetric risk structure in which the family deployed minimal personal capital but still managed to gain enormous upside through token sales, founder allocations and equity stakes.

However, the market dynamics have proven to be completely zero-sum. Data shows that the $2.3 billion taken by the president’s family reflects the $2.25 billion in estimated net losses absorbed by the private and public investors who bought into these companies.

Monetizing the Trump name

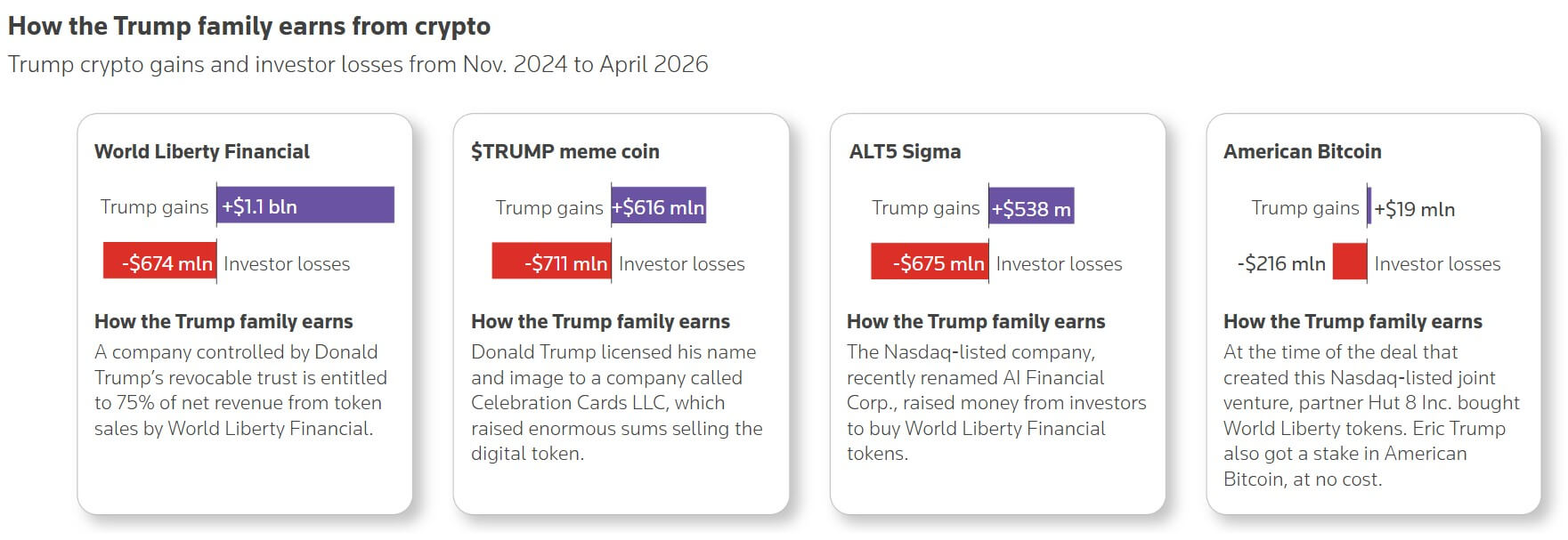

World Liberty Financial was responsible for the majority of the Trump family’s reported crypto income.

The project began selling governance tokens in October 2024, promoting Trump and his sons as central figures. Donald Trump Jr. and Eric Trump traveled to pitch World Liberty’s vision of a financial system beyond traditional banks, as the company positioned itself as a decentralized finance and stablecoin platform.

The economics of the project gave the family a direct claim to symbolic sales revenue. DT Marks DEFI LLC, a business entity linked to the family, secured a contractual right to 75% of the token sale proceeds after fees, netting an estimated $987 million for the family.

That structure allowed the family to collect revenue from the primary token sale, limiting exposure to subsequent market downturns.

However, the token buyers faced a different outcome. Investors in World Liberty suffered losses of around $674 million at the end of April, pressured by long lock-up periods and a sharp drop in value after the token’s listing.

Meanwhile, a similar pattern emerged with the TRUMP meme coin. Launched shortly before Trump’s second inauguration, the token became a speculative vehicle tied to the president’s political brand, rather than an asset with a clear underlying utility.

Blockchain analysis of exchange transfers suggested that the project generated more than $1.2 billion in total revenue, including an estimated $616 million for the Trump family.

Like WLFI, retail buyers absorbed the losses as the token fell from a high of $75.35, leaving investors with more than $700 million in losses.

Wall Street opened a new route to trading

Trump-linked crypto profits also passed through government companies, expanding the trade beyond tokens and into brokerage accounts.

ALT5 Sigma, a small Nasdaq-listed company now known as AI Financial Corp., became one of the clearest examples. The company raised $750 million by selling new shares and used $717 million to buy World Liberty tokens. Reuters reported that more than $500 million from that purchase flowed to the Trump family through World Liberty’s revenue sharing structure.

The deal gave public market investors indirect exposure to World Liberty through a publicly traded stock. Eric Trump and Donald Trump Jr. later rang the Nasdaq’s opening bell after the transaction was completed, making the token purchase a Wall Street event.

The stock subsequently collapsed. Reuters reported that ALT5’s stock price fell from more than $9 in August 2025 to 75 cents at the end of April, causing investors to lose about $675 million.

The family’s economics were separate from that decline, as its profits came from World Liberty’s sale of tokens to ALT5. Outside shareholders bore the risk of a declining share price of the listed company.

American Bitcoin offered another channel into the public market. The Bitcoin mining and treasury company backed by Donald Trump Jr. and Eric Trump, was listed on Nasdaq in 2025.

Reuters reported that the Trump brothers received shares of US Bitcoin at no monetary cost. Eric Trump’s stake was still worth more than $70 million at the end of April, even after a sharp decline in the stock price. Donald Trump Jr.’s Commitment has not been disclosed.

Outside investors again absorbed the losses. U.S. Bitcoin stocks fell from $11 at their launch in September to $1.15 at the end of April, Reuters reported, losing investors more than $200 million.

The deals with publicly traded companies expanded the reach of Trump’s crypto business, as investors who might never have directly purchased a meme coin or governance token could gain exposure through common stock.

The result, however, was the same financial split: Trump-linked entities captured value early, while public investors remained exposed to falling market prices.

Ethical questions follow the money

These market maneuvers take place against a complex regulatory backdrop. The current administration has actively advocated for digital assets, pushed stablecoin legislation and directed federal agencies to adopt a “light-touch” framework.

While this macro policy pivot has undeniably benefited the broader crypto sector, the First Family’s immediate financial windfall has raised unprecedented ethical alarms.

Watchdogs argue that while the mechanisms of these corporate maneuvers appear strictly legal under current law, they represent a deep conflict of interest that generates money for an industry that the executive branch is actively deregulating.

This intersection of policy and personal gain has led to a fierce legislative backlash.

Democratic lawmakers, led by Senator Elizabeth Warren, have petitioned agencies like the CFTC and SEC, arguing that the government’s deep financial entanglements in crypto and prediction markets seriously compromise federal regulation, subordinating public protections to the president’s personal balance sheet.

However, the White House continues to categorically reject these allegations, stating that the administration’s sole purpose is to secure US dominance in the global digital asset race.

World Freedom representatives have similarly pushed back, portraying the protocol as a purely private fintech venture rather than a political vehicle.

But beyond the partisan rhetoric, the ledger is remarkably clear. By treating the presidency as a premium licensing asset, the Trump family has executed one of the most efficient capital extraction strategies in modern financial history, leaving a trail of underwater investors holding the bill.