NFT trading activity showed signs of life in the third quarter of 2025, breaking a long period of decline that defined the post-hype years.

After two years of downsizing and shifting narratives, on-chain markets found new footing, not in high-end collectibles or speculative art, but in cheaper rails, loyalty programs, and sports-related assets traded more by utility than status.

NFT trading volume increased in the third quarter of 2025 and sales peaked.

The focus shifted to lower-cost rails and utilitarian use cases as Ethereum’s scaling pushed activity to L2s, Solana leaned on throughput and compression, and Bitcoin inscriptions grew into a collecting culture that waxes and wanes with fee markets.

Cost and distribution, not profile pictures, now determine the boundaries for growth.

The post-Dencun economy has reset the map. Ethereum’s EIP-4844 lowered data costs for rollups, pushing L2 transaction fees toward pennies and enabling gasless or sponsored flows for mainstream-focused mints.

L2 rates have fallen by more than 90 percent as a result of the upgrade, a shift that is already visible in coin behavior and Base’s emergence as a distribution rail.

On Solana, compression put mass issuance within reach for loyalty and access use cases, with provisioning fees for 10 million compressed NFTs around 7.7 SOL and median transaction fees of almost $0.003, even under tax.

Bitcoin inscriptions have blazed a distinct path tied to mempool cycles and miner revenues, with over 80 million inscriptions as of February 2025 and a top three position based on lifetime NFT sales.

The demand side is showing a recovery, with one caveat.

Data from DappRadar shows that NFT trading volume nearly doubled quarter-on-quarter to $1.58 billion in the third quarter, while sales reached 18.1 million, an all-time high for the number of transactions.

Sports NFTs stood out, with revenue up 337 percent quarter-over-quarter to $71.1 million, a sector where plannable utility, access and loyalty benefits drive spending regardless of minimum pricing. Summer provided a snapback before a cooldown.

Monthly revenue reached $574 million in July 2025, the second-highest month of the year, and then fell about 25 percent month-on-month in September as broader crypto risk appetite declined, based on figures from CryptoSlam.

The pattern reinforces a lower average sales value regime and shows how GMV follows the crypto beta even as unique users and utility categories hold.

Distribution, not just reimbursement, is doing more of the work. Wallets with built-in access keys and sponsored fees remove the entry friction that stalled previous cycles. Coinbase Smart Wallet supports passkeys and gas sponsorships in supported apps, and Phantom reported 15 million monthly active users in January 2025, a base that leads to mobile and social coin funnels.

These things are achieved in chains where cultural and social flows come together. Basic is an example of this.

Base overtook Solana in NFT volume this year as cheap mints, Zora’s mass mint cadence, and Farcaster-adjacent funnels piled up. The tilt explains why creators weighing where to go next start with distribution math and then go back to compensation profiles.

Royalties no longer anchor the revenue stack.

Creator compensation has collapsed since peaks in 2022 after market wars made royalties optional in much of the market. According to Nansen, royalty revenues hit a two-year low in 2023 and did not recover to previous levels.

The countertrend is the rise of enforcement-oriented locations. Magic Eden and Yuga Labs launched an Ethereum marketplace in late 2023 that enforces creator royalties and builds a protected lane for brands that can control it.

The equilibrium is a divided market, with low take rates and primary sales, IP deals and retail tie-ups providing the most margins for creators, while walled gardens absorb premium declines where enforcement is contractual.

Market share remains fluid, where incentives drive order flow. On Solana, Magic Eden and Tensor trade in a duopoly that alternates between reward schemes and program design, with shares often ranging from around 40 to 60 percent for each of the periods.

This is less a structural change than a function of stimulus windows, which can make stock charts look like a regime change that is later reversed. The message for creators is to negotiate distribution as part of launch planning, rather than limiting themselves to a single location.

The short-term roadmap tells us where users actually went.

Sports, ticketing and loyalty programs are expanding because the benefits are plannable and recurring, and the primitive, token-gated access on the chain is already embedded in the existing ticketing and e-commerce flows.

DappRadar’s Q3 breakouts show sports volumes outpacing the market, and that’s before season-long or league-wide programs land.

Gaming is quieter. Immutable’s zkEVM stack and live metrics show steady transaction growth and a security-on-ETH, UX-on-L2 design that aligns with asset custody and recurring fringe fees, Messari said.

IP and licensing are the other bridge from JPEGs to consumer channels. Pudgy Penguins’ expansion to more than 3,000 Walmart stores created a live pipeline from NFTs to physical retail and licensing cash flows.

For creators deciding where to ship next, the cost and UX per chain are now readable. ETH L1 continues to feature art of high quality and provenance, with variable gas prices and optional royalties in most locations.

ETH L2s offer cent-level fees after Dencun, plus sponsored or gasless flows and social funnels on Base and Farcaster.

Solana’s compression brings millions of mints within dollar-level budgets with mobile-first wallet reach. Bitcoin inscriptions correspond to scarce collectibles, where price spikes are a feature and not a bug. The table below summarizes the current journey from coin to trade.

The macro mix is also changing.

An annualized run rate of $5 to 6.5 billion in 2025, with average sales values in the $80 to $100 range in the first half, provides the base from which next year’s scenarios extend.

Using CryptoSlam’s monthly sales as a backbone and splitting the DappRadar category by color, a bear case comes out to $4-5 billion GMV if the crypto beta stalls and average sales values decline, with fee-sensitive use cases focusing on Solana and ETH L2s, ETH L1 art stable, and inscriptions that the Bitcoin fee cycles follow.

A base case in the $6-9 billion range requires built-in wallets and social coin rails to continue expanding, plus sports and live events expanding across seasons and brands testing royalty-mandated locations for new drops.

The $10 to 14 billion bull case would require a step change in mobile distribution, with Base and passkeys normalizing coin flows, Phantom monthly actives rising above 20 million, ticket pilots transitioning to regular programs, and gaming assets returning.

In all three bands, the stock mix tilts toward ETH L2 and Solana, with ETH L1 narrower and Bitcoin stable as a collectibles lane.

Six switches will determine how quickly that current manifests.

- Wallet UX and distribution will be the leading indicator, measured by key acceptance, sponsored fees, and MAUs for Phantom and Coinbase Smart Wallet.

- The footprint of royalty enforcement matters for bounty declines, including any OpenSea policy pivot points and the health of creator-affiliated markets on Ethereum.

- Sports and ticketing partners moving from pilots to seasonal programs are converting one-time GMV into schedules.

- Base and Zora’s cadence, visible in monthly mints and Base’s share of NFT GMV alongside Farcaster Frames, shows whether social funnels will hold up.

- The adoption of Solana compression, tracked by compressed coin counts and cost per million assets, indicates whether loyalty and media programs are moving from experimentation to standards.

- Bitcoin fee cycles, and their link to inscriptions and Runes, will continue to drive collectibles prices as mempool congestion ebbs and flows.

Two risks remain constant. Wash trading and spamminting still distort GMV and sales counts. Therefore, it is safer to look at average sales values and organically filtered dashboards.

Market stimuli can make stock charts look like a regime change when it comes to just airdrop cycles, especially in the Solana duopoly, so launch plans need to price this in from the start. The other operational constraint is revenue design.

Because royalties in open markets are usually optional, primary sales, IP licensing and retail bear a greater share of the burden, while forced locations create a premium lane that some brands can tap into and most cannot.

What looked like an end state in 2023 turned into a migration.

The JPEG boom is over, the rails have gotten cheaper, the use cases now match tickets, sports, gaming and IP, and the wallet and distribution stack is starting to meet users where they already are.

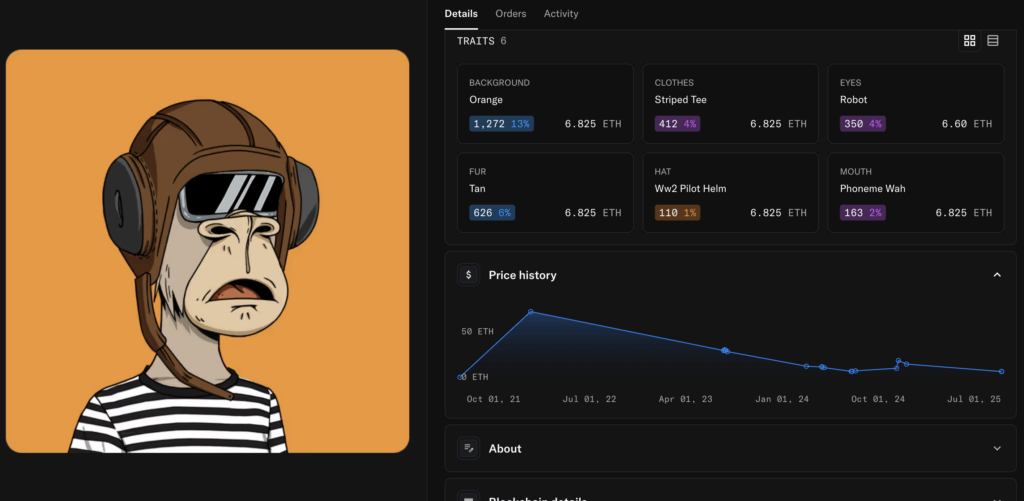

The Blue Chip flagship NFT, Bored Ape Yacht Club, is still in a perilous state for those who have invested six figures in AWS-hosted JPEGs. The NFT below sold for over 74 ETH in 2021, but is now worth just 9 ETH, down 87 percent in three years.

Speculation about the non-fungible sector may be over, but will it finally allow the underlying technology to gain traction in real-world utility applications? Only time will tell, but the signs are promising, just not for the bag holders.

The third quarter ended with $1.58 billion in transactions and 18.1 million sales, and the mix is already moving in that direction.