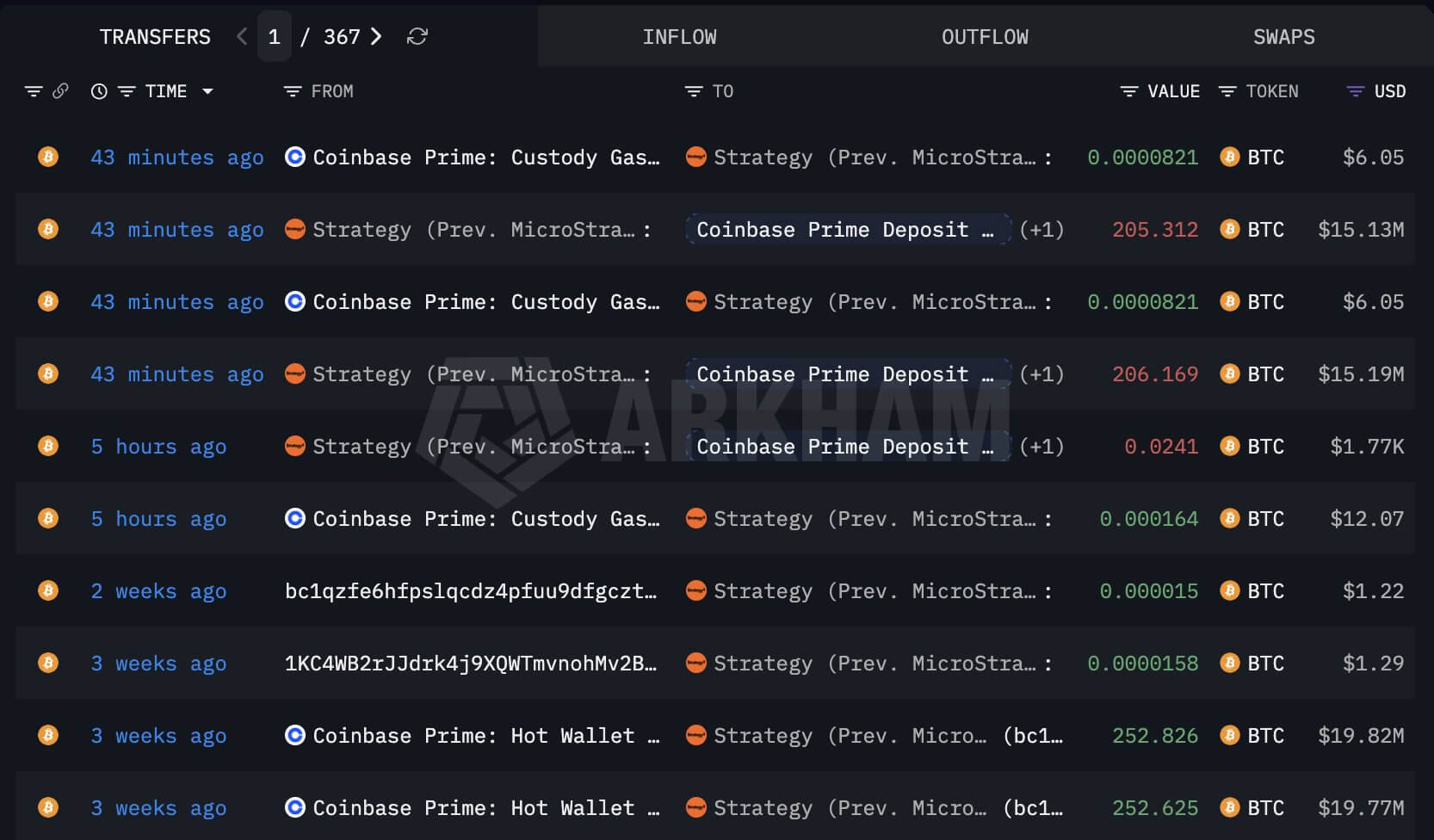

On May 29, Strategy (formerly MicroStrategy) moved more than 411 Bitcoin to Coinbase Prime, putting Michael Saylor’s funding model under renewed scrutiny.

Data from Arkham Intelligence showed two transfers of approximately 205.3 BTC and 206.2 BTC from Strategy-linked wallets before the coins reached the destination address.

This move has not been confirmed as a sale, and Strategy has previously shifted coins between wallets as part of custodial management, prompting similar speculation that later appeared to reflect an internal restructuring.

However, the last transfer attracted more attention because of the way the coins moved.

ForeDex Proof, a supply chain analyst, said the transferred Bitcoin first left two Strategy-linked wallets for new addresses before being moved again, a second step that differs from previous wallet migrations.

These previous transfers typically stopped after the funds were moved from an MSTR-linked wallet to a new address.

Moreover, the address format also stood out. ForeDex Proof said Strategy has historically used Coinbase Custody and Native SegWit addresses starting with “bc1q,” while the latest move involved an address starting with “3,” a P2SH format.

Taking this into consideration, the analyst said the latter wallets appeared to be linked to Coinbase Prime activity usually associated with over-the-counter transactions, raising the possibility that Strategy was preparing to sell a small portion of its holdings.

Still, this BTC move represents only a fraction of Strategy’s 843,738 BTC treasuries, but the timing gave the move more weight.

This is because it happened in a week in which the company paused new Bitcoin purchases, started buying back convertible debt and told investors that selling Bitcoin could become part of its financing toolbox if market conditions or dividend obligations required it.

STRC stress reduces the room for error in the strategy

The Coinbase-linked transfer comes as Strategy’s preferred share structure is under pressure from a declining dollar reserve and weaker trading in STRC, the preferred floating rate instrument designed to trade around its $100 par value.

In recent months, Strategy has used the issuance of preferred stock as part of a broader financing system that allows it to raise capital, buy Bitcoin and manage liabilities without relying solely on common stock or convertible debt.

Market observers noted that STRC’s structure depends on market confidence, as investors must believe the company can continue to pay dividends, maintain adequate cash coverage and access capital markets.

That confidence has become more fragile because STRC has consistently traded below par since mid-month.

Meanwhile, Strategy recently moved to repurchase nearly $1.5 billion in face value of its 0% convertible senior notes due 2029 for approximately $1.38 billion in cash.

The buyback eliminated a future liability and retired the notes at a discount, but it also reduced the reserve that some investors had seen as a cushion for preferred dividends and interest costs.

Glenn Cameron, global head of institutional at Onramp Bitcoin, said Strategy’s dollar reserve fell from $2.25 billion on February 1 to $871 million on May 25. The decline roughly corresponded to the cash costs of convertible bond repurchases.

Cameron estimated that Strategy’s annual cash obligation is about $1.66 billion, including preferred dividends, convertible interest and burning software companies. He said STRC alone accounts for about $1.23 billion of that total, at a dividend rate of 11.5%.

By that estimate, Strategy’s remaining dollar reserve covers approximately 6.3 months of annualized liabilities. Cameron said the reserve had been offered to STRC subscribers to cover about 2.5 years of preference dividends and interest on debt before the convertible bond buyback reduced the cash cushion.

These figures heighten concerns about the company’s financing structure. If STRC continues to underperform, Strategy may need to increase the dividend rate to restore demand, and any increase will apply to the entire outstanding STRC stack, increasing the company’s future cash burden.

Crypto analyst Ragnar said Strategy needs to replenish its cash reserves as quickly as possible and argued that STRC’s weakness could reflect investor concerns about its shrinking funding ratio.

He said the company could sell higher-priced Bitcoin lots to rebuild cash, citing purchases of 220 BTC for $123,561, 430 BTC for $119,666 and 6,220 BTC for $118,940 as potential candidates if Strategy chooses to reduce margin exposure.

That theory would fit the logic of a tactical sale without changing Strategy’s broader interests. Selling higher-priced coins could raise cash and lower the company’s average cost base, while keeping most of its coffers intact.

It would also mark a visible change in the way investors understand Saylor’s Bitcoin strategy, as even a limited sale would demonstrate that some coins can be used to shore up the capital stack when market conditions tighten.

The strategy has a period of four months

Joao Wedson, CEO of Alpharactal, said the pressure reflects a deeper problem around Strategy’s accumulation timing.

He argued that a company with such a large Bitcoin position should have achieved a much lower average entry price during the 2022 and 2023 bear market period, rather than maintaining an average purchase price of around $70,000 after aggressive buying in 2024 through 2026.

Wedson said older Bitcoin holders were distributing during Strategy’s later phase of accumulation, giving the company a less favorable risk-reward profile.

His criticism hits at one of the assumptions behind the model: that repeated capital increases can continue to improve shareholder exposure as long as the company converts proceeds into Bitcoin.

That argument has become more relevant as preferred dividends grow. A lower average cost basis would give Strategy more flexibility to sell a limited amount of Bitcoin and still realize treasury profits.

However, a higher cost base leaves less room between the market price, investor confidence, and the liabilities associated with the company’s pile of preferred stock.

Jeff Dorman, head of investments at Arca, said Strategy has made its first major bond between common shareholders, Bitcoin holders and preferred investors.

He argued that the company could have kept its cash cushion for dividend payments, but instead used much of that reserve to pay down 0% of its debt.

Dorman said the company now faces two main roads if the pressure continues. It can sell Bitcoin to help fund preferred dividends, supporting preferred holders while weakening the accumulation story. Or it could stop paying dividends, preserving the Bitcoin pile and undermining confidence in the preferred securities.

Strategy could also attract new capital, but that depends on market access. STRC’s design is based on the ability to issue securities at near par. If investor demand weakens, the company may have to offer higher returns to attract buyers, increasing future liabilities against the same Bitcoin pool.

Dorman said tensions could increase over the next four months. That timeline has become a test of whether Strategy can keep its funding circuit intact while Bitcoin remains volatile, STRC trades below par and the dollar reserve offers less room for error.