Arca CIO Jeff Dorman warned that Strategy’s Bitcoin-heavy balance sheet has entered a more dangerous phase, arguing that the company, Bitcoin holders and its favored shareholders are now stuck in a difficult trade-off between capital structures.

On May 28 after on His central concern is not simply Strategy’s Bitcoin exposure, but the layering of preferred stock obligations, cash management decisions, and potential pressure to ultimately sell BTC if market conditions deteriorate.

Arca CIO Warns MSTR Is Facing Bitcoin Crunch

Dorman said Strategy could have avoided much of the current tension by slowing down after the initial Bitcoin accumulation strategy became a dominant part of the company’s identity. “MSTR couldn’t have done anything before they started pumping out billions in preferences,” he wrote, adding that such a path “would have made MSTR boring” but more stable.

Related reading

Instead, Dorman argued, the company’s push for preferred stock seemed to rest on an aggressive assumption that Bitcoin was about to move sharply higher. “The push for these preferences was based on the fact that he clearly thought BTC was about to boom – I wasn’t sure what he saw to think that,” Dorman wrote, pointing to possible explanations such as the four-year cycle or the money flows. “But that’s the only reason to take those kinds of miscalculated risks to mess up his balance sheet so badly – he must have thought BTC was about to take off and that he could easily pay the pref dividends with future BTC sales.”

The problem became more acute, according to Dorman, when Bitcoin started to decline. He said the market was getting nervous because Strategy’s roughly $15 billion in preferred bonds yield about $1.5 billion in annual dividends. In response, Dorman said the company has raised $2 billion in cash through a stock issuance, a move he characterized as a way to ease concerns about near-term defaults and buy “almost two years of runway” to cover dividends.

Dorman called raising cash a “smart move” but said the subsequent decision to use the buffer to buy back bonds due in 2029 was difficult to understand. “But then for some unknown reason he decides to use that cash cushion and buy back bonds due 2029 instead of using them to finance the annual dividends,” he wrote. “This is a baffling decision for a company with cash flow problems. Why would you pay off a 0% coupon debt with the only cash you have?”

Bond buybacks could make a small contribution because they were done at a discount, Dorman acknowledged. Still, his point was that the company appeared to be devoting scarce liquidity to long-term, zero-coupon debt, while the preferred dividend burden remained the most immediate constraint.

Dorman also left room for the possibility that Michael Saylor, executive chairman of Strategy, has another capital markets maneuver in mind. “The only bull case is that underestimating Saylor’s deception in the capital markets has been a losing proposition for years. Maybe there was a plan?” he wrote.

One possibility, Dorman said, is that the company could refinance the converts with new longer-term convertible notes, although he noted that Saylor has “sworn off converts,” making that outcome less likely in his view. Another option is to sell Bitcoin to fund preferred dividends, but Dorman described this as a potential negative outcome for both MSTR and BTC if this were to happen during a sharper market decline.

When asked by an X user what the way out is, Dorman gave two basic scenarios. “Sell BTC to pay the prefs – bad for MSTR, bad for BTC, good for STRC,” he wrote. “Stop paying the dividend on the prefs – good for BTC, good for MSTR, bad for STRC. Those are really the only answers at the moment.”

Dorman also said that neither he nor Arca is short MSTR, after another user asked if his company had a bearish position.

His conclusion was stark: This is the first time that MSTR, Bitcoin and preferred holders are “really in a pinch.” According to Dorman, the coming months could force a choice between preserving liquidity, protecting Bitcoin exposure and keeping preferred shareholders intact, a choice that could cause serious pain to at least one group of stakeholders.

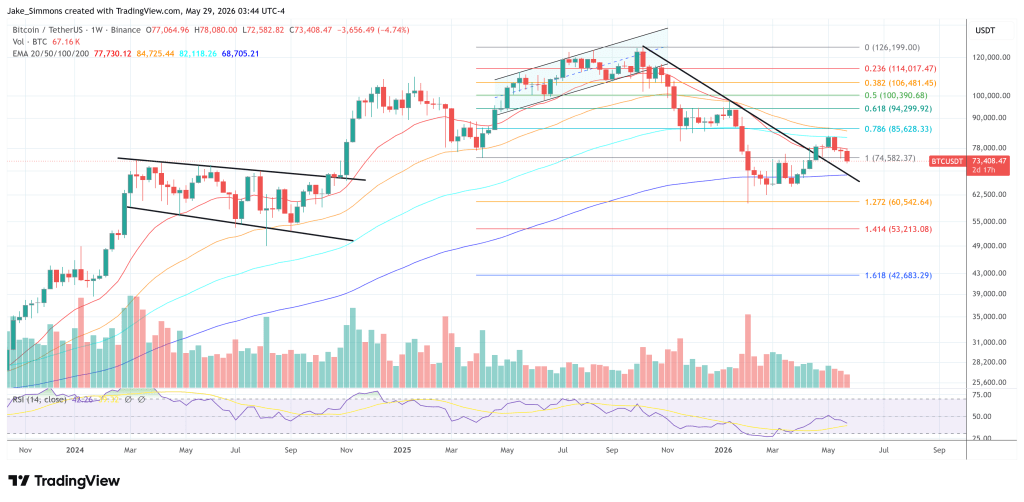

At the time of writing, BTC was trading at $73,408.

Featured image created with DALL.E, chart from TradingView.com