Asset manager Grayscale says small group of blockchains already dominate decentralized finance (DeFi) and tokenized assets Ethereum, Solana $BNB Chain and Canton Network are best positioned to absorb the first wave of institutional capital once the United States passes the CLARITY Act, the long-promised crypto rulebook.

The CLARITY Act cleared the Senate Banking Committee for a 15-9 vote on May 14. Now it requires a full vote in the Senate, reconciliation in the House of Representatives and a presidential signature.

However, the current calendar poses another limitation. In a May 21 post, Cryptopolitan reported that the bill will now compete for floor time in June with reconciliation, the Foreign Intelligence Surveillance Act and the housing bill passed by the House this week.

Which networks do Grayscale think will absorb the first wave of institutional capital?

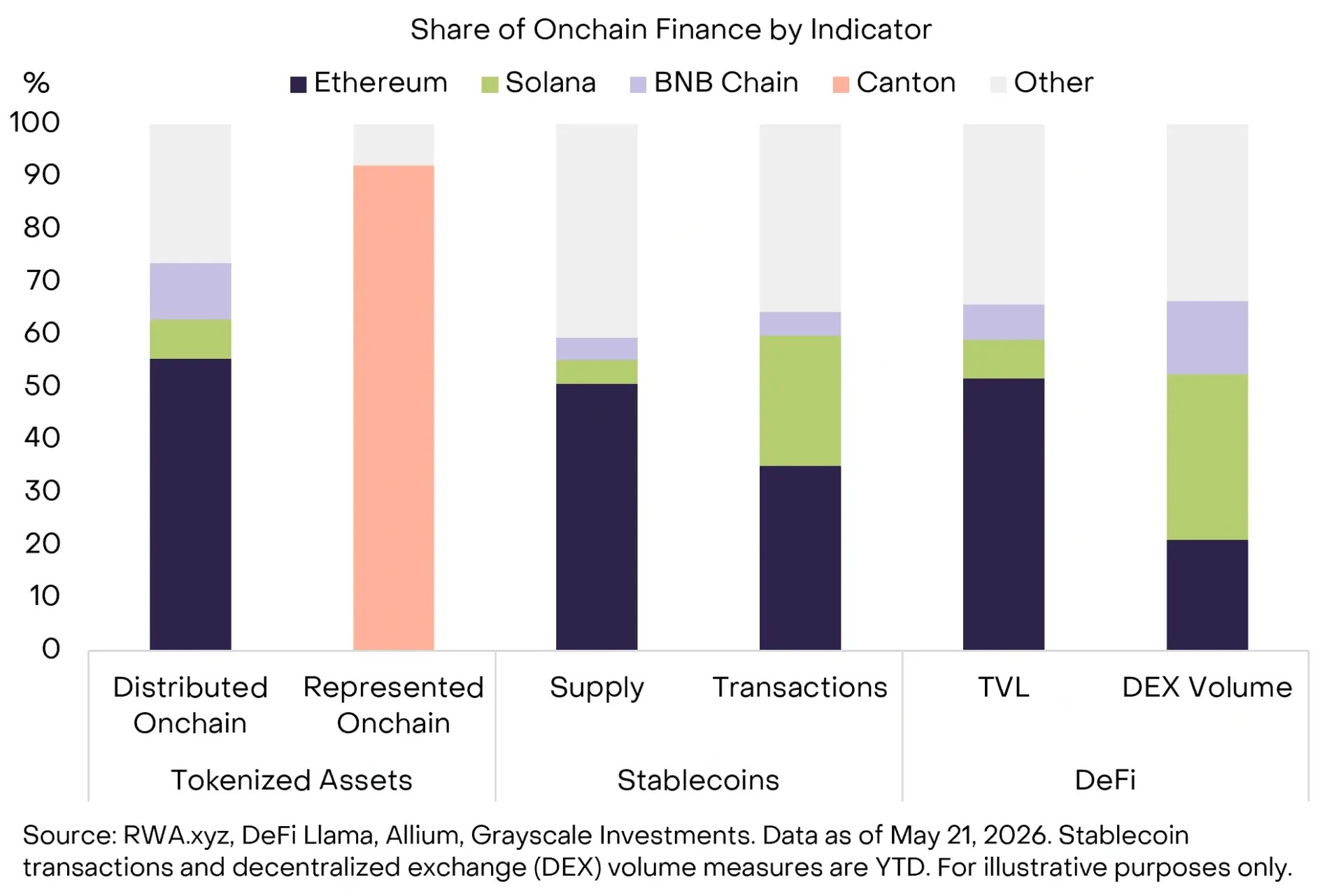

Ethereum currently leads on tokenized assets with full on-chain functionality, followed by $BNB Chain and Solana.

Canton Network has also made a name for itself as a dominant institutional niche. According to Grayscale’s before tokenization megatrend reportCanton leads all blockchains in total on-chain capital with more than $348 billion in tokenized asset value, anchored by DTCC’s selection of the network under the SEC’s No-Action Letter framework.

The same blockchains also differ in terms of supply and transaction volume when it comes to stablecoins. The current TVL in DeFi is round $82.08 billionand Ethereum, Solana and $BNB Chain is responsible for most of it. They also lead in application activities.

Grayscale highlighted a list of secondary platforms including Avalanche, Ethereum Layer 2 networks Base and Arbitrum, the perpetuals-focused Hyperliquid and the stablecoin-heavy Tron as likely beneficiaries.

Zach Pandl, Grayscale’s head of research, pointed out that while Bitcoin does not natively support smart contracts and has a more limited Layer 2 ecosystem, it will still benefit from regulatory clarity as the industry’s most secure asset and leading collateral.

When will the CLARITY Act be passed, and what could derail it?

According to Crypto in America podcast host Eleanor Terrett, “The reality of whether the Senate can get two major pieces of legislation done amid time constraints and competing priorities is beginning to emerge, and questions are now being asked as to whether a July will inevitably slip in.”

She pointed out that there are four work weeks in June and three in July, before the August recess.

Senator Cynthia Lummis has called a June vote likely quite optimistic.

DeFi could also get a regulatory boost

While these deliberations are still ongoing, the SEC has not waited. On March 17, the agency issued a joint interpretation with the Commodity Futures Trading Commission (CFTC) establishing a coherent definition and classification for digital commodities, collectibles, tools, stablecoins and digital securities.

It also clarified how an unsecured crypto asset can become subject to or cease to be subject to an investment contract, while also addressing airdrops, protocol mining, staking and packaging of unsecured assets.

SEC Chairman Paul S. Atkins said, “This effort serves as an important bridge for entrepreneurs and investors as Congress works to advance bipartisan market structure legislation, which I look forward to implementing with Chairman Selig in the near future.”

The DeFi space is also making an effort to clarify regulations. As Cryptopolitan reported in April, the DeFi Education Fund (DEF) and 35 other co-signatories urged the Securities and Exchange Commission (SEC) to enact its staff guidelines on DeFi interfaces into law so that they cannot be rolled back once a new regime comes into place.

In its current form, the Guidelines are merely an interim staff statement that will be considered withdrawn five years after the date of publication unless the Commission determines otherwise or makes it a rule.

The SEC Division of Trading and Markets staff statement issued on April 13 clarifies that certain operators of crypto trading interfaces are exempt from registering as broker-dealers.