- Massive accumulation of Bitcoin by institutions as retail investors panic.

- USDT dominance bearish reversal pattern to trigger Bitcoin rally.

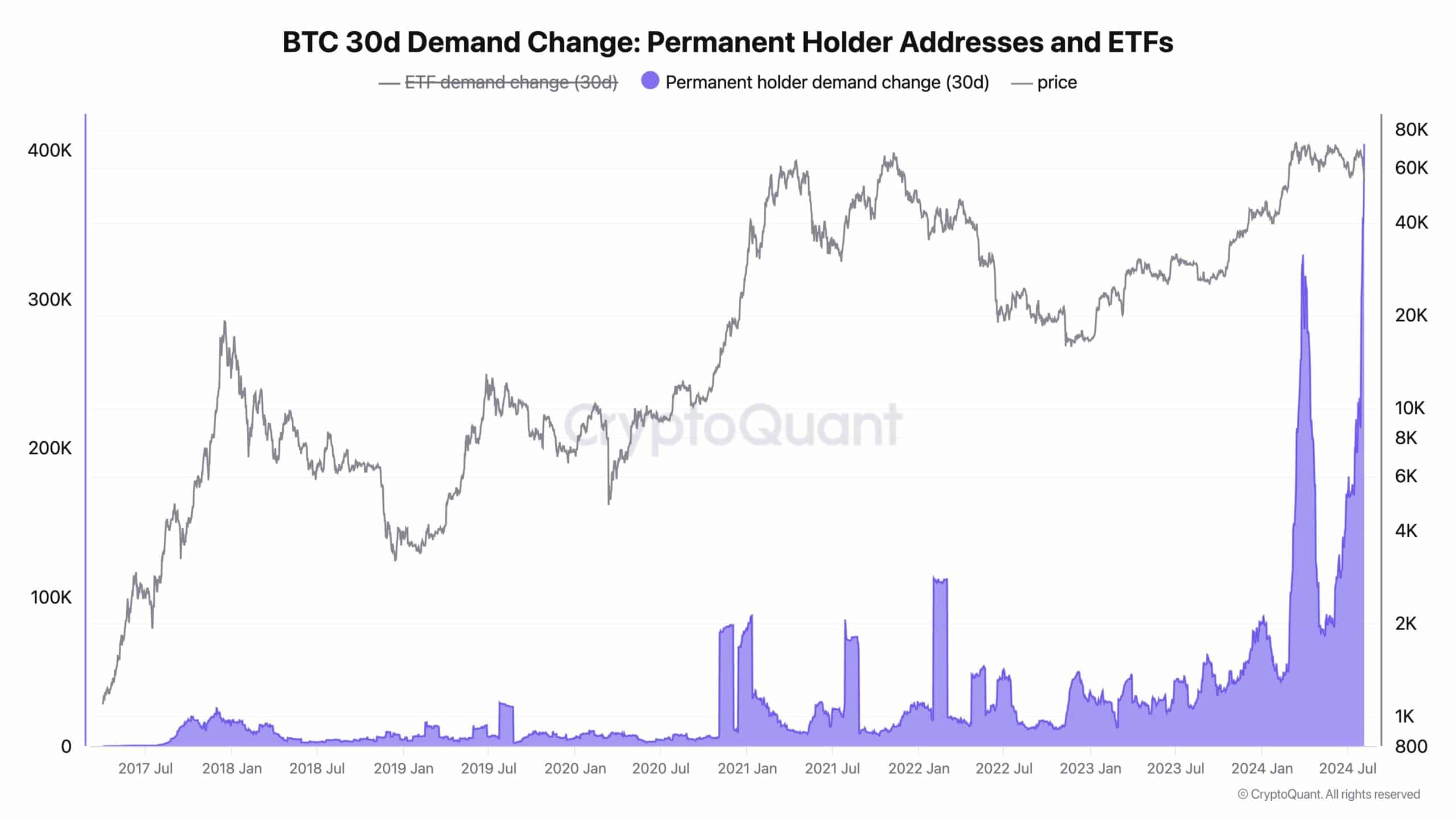

404,448 Bitcoins [BTC]worth $23 billion, have been moved to permanent addresses of holders over the past 30 days, according to the chain’s data, indicating significant accumulation.

Private investors, distracted by concerns such as the German government sell-off or the Mount Gox issues, may regret not buying the dip. This missed opportunity is highlighted as institutions are believed to have bought during the recent market dip.

Source: CryptoQuant

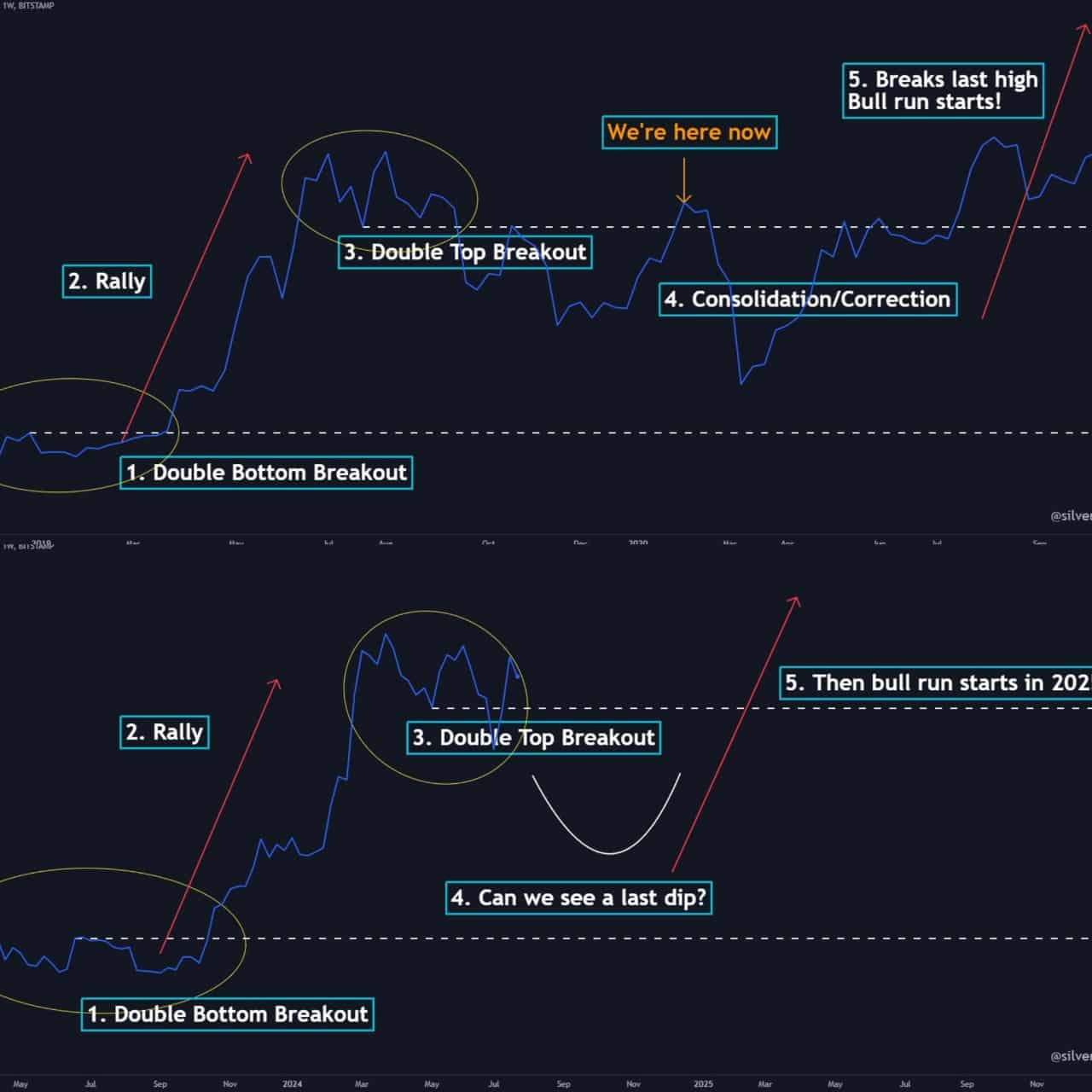

The weekly BTC chart reflects the 2019/20 BTC cycle

For weeks, warnings have emerged about investors and traders becoming too optimistic and ignoring signals on the weekly BTC chart.

This year’s chart resembles the 2019-2020 cycle and shows a double bottom, a peak with a double top, a break, a low and then a rally.

Currently, BTC is in a correction phase and may be experiencing its last dip before a new rally. This phase has attracted significant institutional investment, with many Bitcoins moving to permanent holding addresses.

Do we see history repeating itself?

Source: TradingView

USDT’s dominance is declining, Bitcoin is rising

When USDT’s dominance wanes, crypto prices often rise. This became clear on ‘Crypto Black Monday’, when $1.7 billion in assets was liquidated.

USDT’s dominance tested a key resistance and was rejected, signaling a possible shift in the direction of the market.

The 50-day exponential moving average was also retested, confirming the trend reversal. This event highlighted the high volatility of the crypto market and the risks associated with it.

Source: TradingView

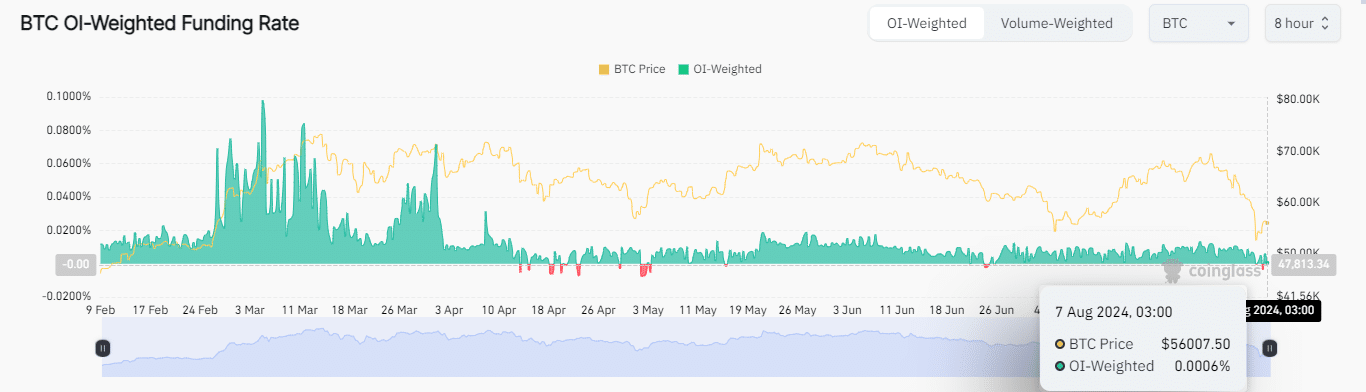

Bitcoin’s volume-weighted funding rate versus institutional purchases shows discrepancies

Divergence occurs when two related measures move in different directions, signaling a possible market reversal.

Is your portfolio green? Check the Bitcoin Profit Calculator

A falling Bitcoin funding rate indicates a bearish trend, but heavy institutional buying exceeding retail sales signals a possible reversal.

This market correction could last four to eight weeks, followed by a potential rally in the third quarter of 2024.

Source: Coinglass